A global markets summary, for

Australian investors

US payrolls missed sharply at 57K this week, driving the dominant market move, while European disinflation continued and Australian building approvals declined, painting a mixed but broadly constructive picture for global and domestic markets.

Five key developments:

1. US JOLTS Job Openings rise to 7.59M vs 7.28M expected

US job openings unexpectedly increased to 7.59 million, reinforcing the view that labour demand remains resilient despite signs of broader economic moderation. While hiring has slowed in recent months, the data suggests businesses are still actively seeking workers, supporting consumer spending and reducing immediate recession concerns. Markets interpreted the result as slightly hawkish for Federal Reserve expectations, although softer payroll data later in the week moderated that view.

2. European Core CPI declines to 2.4%

European Core CPI eased to 2.4%, continuing the gradual disinflation trend across the Eurozone. The result strengthens expectations that inflation is steadily returning towards the European Central Bank’s target, providing policymakers with additional flexibility to maintain an accommodative stance. Lower inflation supports consumer purchasing power and business confidence, although economic growth across Europe remains relatively subdued.

3. US ISM Manufacturing PMI steady at 53.3

The US ISM Manufacturing PMI remained steady at 53.3, indicating the manufacturing sector continues to expand despite ongoing global uncertainty. Readings above 50 signal improving business conditions, with production, new orders and employment remaining relatively resilient. Stable manufacturing activity offsets some concerns around slowing employment growth and suggests the broader US economy continues to expand at a moderate pace.

4. US Non-Farm Employment Change declines to 57K vs 129K previous

US employment growth slowed sharply, with Non-Farm Payrolls increasing by just 57,000 jobs compared to the previous month’s 129,000. The weaker labour market data suggests higher interest rates are beginning to weigh on hiring activity and may increase the likelihood of Federal Reserve rate cuts later this year. Financial markets welcomed the softer data, as easing labour market pressures reduce inflation risks without necessarily signalling an imminent recession.

5. Australian Building Approvals m/m decline by -1.1%

Australian building approvals fell 1.1% over the month, highlighting ongoing weakness across the construction and residential housing sectors. Elevated borrowing costs, labour shortages and higher construction costs continue to weigh on new project commencements. While housing supply remains structurally constrained, softer approvals suggest residential construction is likely to remain subdued over coming quarters.

Australian Focus

US payrolls came in at just 57K against expectations of 129K, the week’s standout result, with markets welcoming the softer labour data as reducing inflation pressure without pointing to recession. European core CPI easing to 2.4% added to the disinflation narrative, while US manufacturing holding steady at 53.3 and job openings remaining elevated at 7.59M rounded out a picture of an economy slowing gradually rather than sharply.

For Australian investors, the constructive global tone supported gains across healthcare, financials and selected resources on the ASX, with banks well bid and CSL leading healthcare higher. The domestic note of caution came from building approvals falling 1.1%, a further sign that elevated borrowing costs continue to weigh on residential construction activity and new project commencements.

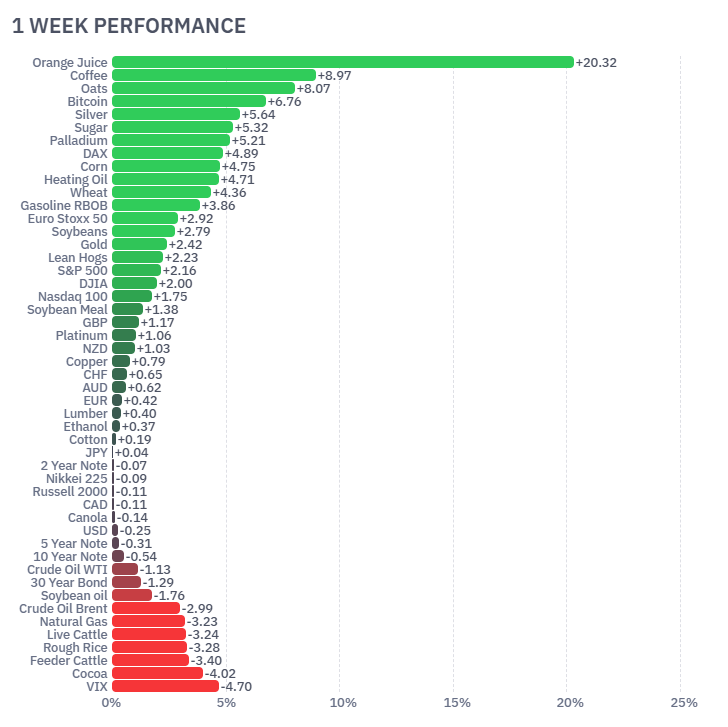

Futures Market Performance

Global markets delivered another constructive week, led by strength across agricultural commodities, industrial metals and equities. Orange Juice surged (20.32%), while Coffee(+8.97%), Oats (+8.07%) and Bitcoin (+6.76%) also posted strong gains. Major equity indices including the S&P 500 (+2.16%), Dow Jones (+2.00%), Nasdaq (+1.75%) and DAX (+4.89%) all advanced as softer US employment data increased expectations for future Federal Reserve easing. Energy markets weakened, with WTI Crude (-3.13%), Brent Crude (-2.99%), Natural Gas (-3.23%), while the VIX (-4.70%) declined, reflecting improving investor confidence and lower perceived market risk.

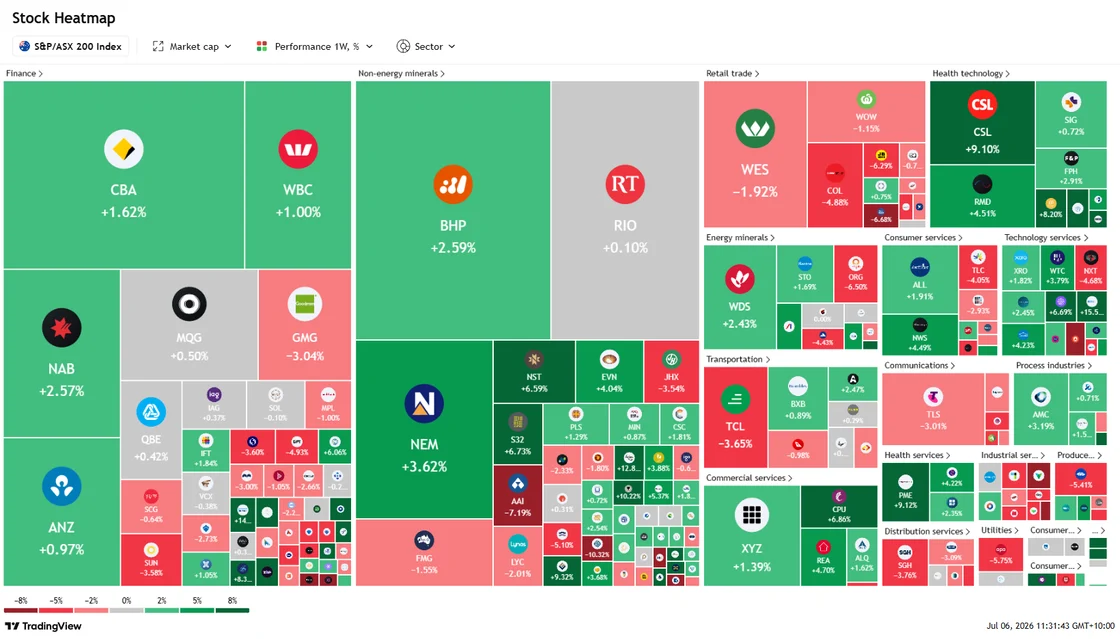

ASX Weekly Heatmap

The Australian market finished the week broadly higher, supported by strength across healthcare, financials and diversified miners. CSL (+9.10%) led the healthcare sector following positive investor sentiment, while Ramsay Health Care (+4.51%) also performed strongly. Banks remained well bid with NAB (+2.57%), CBA (+1.62%), Westpac (+1.00%) and ANZ (+0.97%) providing significant support to the index. Resource stocks were mixed, with BHP (+2.59%), Newmont (+3.62%) and Woodside (+2.43%) offsetting weakness in Fortescue (-1.55%), James Hardie (-3.54%) and Transurban (-3.65%). Consumer discretionary remained under pressure, led by Wesfarmers (-1.92%), reflecting ongoing caution around domestic consumer spending.

If any of this week’s developments raise questions about your portfolio, please get in touch.

Related Insights

Iran's renewed blockade of the Strait of Hormuz reignited energy supply concerns this week, pushing...

The RBA held the cash rate steady at 4.35% this week, supporting Australian equities while the Bank...

The US Iran peace deal dominated global markets this week, rapidly unwinding geopolitical risk premi...