A global markets summary, for

Australian investors

The RBA holds rates at 4.35% this week, providing near-term relief for Australian equities and yield-sensitive sectors while the Bank of Japan’s hike to 1.00% reinforced that global policy divergence remains very much active.

Five key developments:

1. BOJ raises rates to 1.00%

The Bank of Japan raised rates to 1.00%, reinforcing that Japan is continuing to move away from ultra-loose policy settings. The move supported the Yen and added pressure to Japanese equities, with the Nikkei down over the week. For markets, the key takeaway is that global policy divergence remains active, particularly as Japan normalises while other central banks are closer to holding or easing.

2. RBA holds cash rates steady at 4.35%

The RBA held the cash rate steady at 4.35%, keeping policy restrictive while it assesses inflation and labour market conditions. This was broadly supportive for Australian equities, as it reduced near-term concerns around another rate hike. The decision also helped sentiment toward banks and yield-sensitive sectors, with the market continuing to price a more stable domestic rate outlook.

3. British CPI y/y contracts to 2.8%

UK inflation eased to 2.8% year-on-year, giving markets more confidence that price pressures are continuing to moderate. This supported expectations that the Bank of England may have more flexibility to ease policy later in the year. Lower inflation is generally positive for equities, as it reduces pressure on consumers, improves real income trends, and supports lower bond yield expectations.

4. US Fed holds rates steady at 3.75%

The US Federal Reserve held rates steady at 3.75%, maintaining a wait-and-see approach as inflation continues to trend lower but remains a key focus. Equity markets responded relatively positively, with the S&P 500 and Nasdaq finishing higher over the week. The hold suggests the Fed is comfortable pausing for now, which remains supportive for risk assets if earnings momentum holds.

5. NZ GDP q/q climbs to 0.8%

New Zealand GDP rose 0.8% quarter-on-quarter, suggesting the economy is showing signs of resilience after a softer period. Stronger growth helped reduce recession concerns and supported the New Zealand dollar. From a broader market perspective, the result points to a more constructive growth backdrop across the region, although central banks will remain cautious if stronger activity delays inflation normalisation.

Australian Focus

The RBA’s decision to hold rates at 4.35% was the key domestic development this week, removing near-term hike risk and supporting sentiment across banks and yield-sensitive sectors. The board appears comfortable sitting at current settings while it waits for clearer confirmation that inflation is heading sustainably back toward target.

For Australian investors, the hold provides a more stable backdrop, and that played out directly in the ASX with financials and healthcare both performing strongly. Resources tell a different story, with iron ore demand concerns and broad commodity weakness continuing to drag on BHP, Rio and FMG. The broader global picture is gradually improving, with the Fed on hold and UK inflation easing further, but the BOJ hiking to 1.00% is a reminder that policy divergence can still generate sharp moves, particularly for yen-sensitive and globally exposed positions.

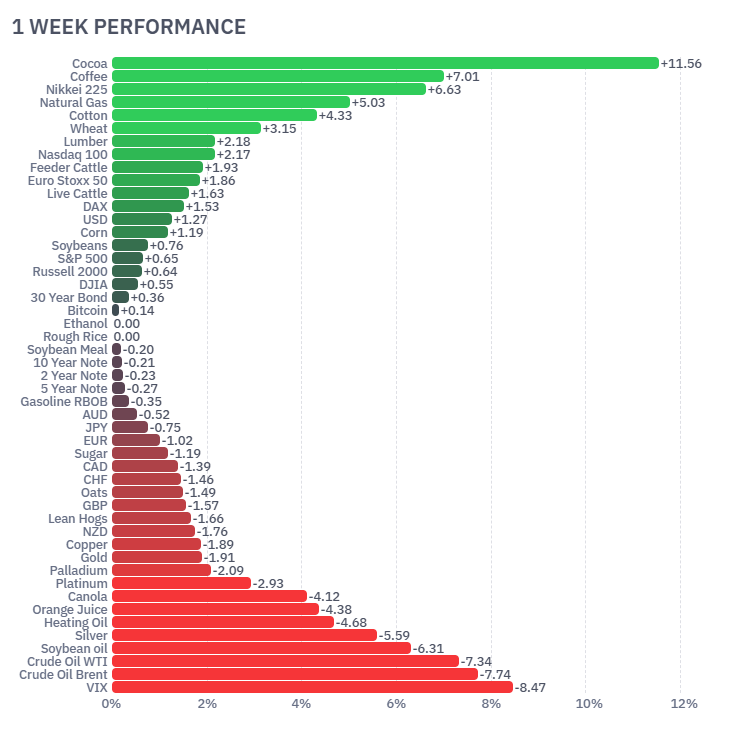

Futures Market Performance

Commodities were mixed but heavily skewed toward strength in softs and weakness in energy. Cocoa surged (+11.56%), while Coffee (+7.01%), Nickel (+6.63%), Natural Gas (+5.03%) and Cotton (+4.33%) also rose strongly. Equity futures were modestly positive, with the S&P 500 (+0.65%) and Nasdaq 100 (+2.17%) higher. Energy was the clear laggard, with Brent (-7.74%), WTI (-7.34%), Heating Oil (-4.68%) and Silver (-5.59%) all weaker. The VIX fell sharply (-8.47%), signalling improved risk appetite.

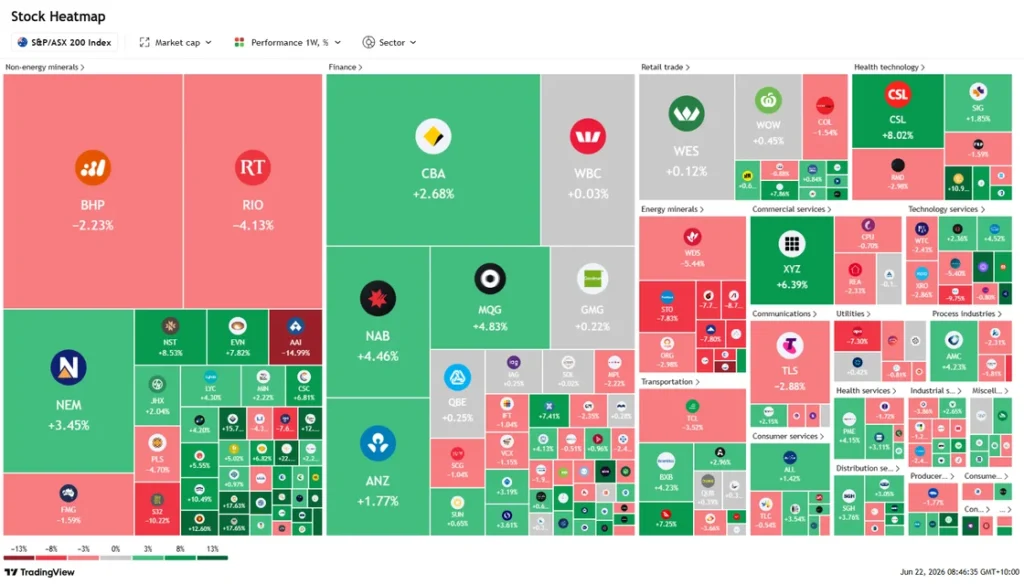

ASX Weekly Heatmap

The ASX 200 was mixed, with banks and healthcare supporting the index while miners and energy weighed on performance. CBA (+2.68%), NAB (+4.46%), MQG (+4.83%) and ANZ (+1.77%) were all stronger, while CSL (+8.02%) provided significant support to the healthcare sector.

Resources were the clear laggards. BHP (-2.23%), Rio Tinto (-4.13%) and FMG (-1.59%) declined as investors became increasingly cautious on the outlook for Chinese steel demand and iron ore prices. Energy stocks were hit particularly hard following a sharp fall in oil prices, with Woodside (-5.44%) and Santos (-7.83%) among the worst performers.

If any of this week’s developments raise questions about your portfolio, please get in touch.

Related Insights

Iran's renewed blockade of the Strait of Hormuz reignited energy supply concerns this week, pushing...

US payrolls missed sharply at 57K this week, lifting rate cut expectations and supporting a broadly...

The US Iran peace deal dominated global markets this week, rapidly unwinding geopolitical risk premi...