A global markets summary, for

Australian investors

The RBA holds rates at 4.35% this week, providing near-term relief for Australian equities and yield-sensitive sectors while the Bank of Japan’s hike to 1.00% reinforced that global policy divergence remains very much active.

Five key developments:

1. Iran blocks Strait of Hormuz again

Iran’s Revolutionary Guard declared the Strait of Hormuz closed after missiles struck and damaged a commercial vessel. The US responded with strikes on Iranian naval and missile targets, while Iran launched missiles and drones toward Qatar, the UAE and Jordan. Shipping continued through the southern channel, but traffic slowed sharply and energy prices rose on renewed supply concerns.

2. RBNZ raises Official Cash Rate by 0.25% to 2.50%

The Reserve Bank of New Zealand increased its Official Cash Rate by 25 basis points to 2.50%, citing persistent inflationary pressures and a resilient domestic economy. Policymakers indicated they remain committed to returning inflation sustainably to target, while acknowledging that higher borrowing costs are likely to weigh on household spending and business investment over coming quarters.

3. US ISM Services PMI steady at 54

The US ISM Services PMI remained unchanged at 54, indicating that the services sector continues to expand at a healthy pace. Business activity and new orders remained resilient despite higher interest rates, reinforcing the view that the US economy continues to avoid a significant slowdown. The result provided further evidence that domestic demand remains supportive of economic growth.

4. US Federal Reserve release minutes showing deep divide

Minutes from the Federal Reserve’s latest meeting revealed policymakers remain divided over the appropriate path for interest rates. While some members expressed concern that inflation risks remain elevated and further tightening may be required, others argued the labour market is softening sufficiently to justify patience. The release reinforced expectations that future policy decisions will remain highly data dependent.

5. Chinese CPI y/y steady at 1.0%

China’s annual inflation rate held steady at 1.0%, highlighting ongoing stability in consumer prices despite mixed economic conditions. The result suggests domestic demand remains modest while avoiding deflationary pressures that concerned markets earlier in the year. Investors continue to watch for additional fiscal and monetary stimulus as Chinese authorities seek to strengthen economic momentum.

Australian Focus

Iran’s renewed closure of the Strait of Hormuz dominated the week, with strikes on a commercial vessel and retaliatory US military action pushing energy prices sharply higher and reviving the supply disruption risk that markets had begun to price out following the June peace deal.

For Australian investors, the energy shock feeds directly back into the inflation outlook at a delicate moment. The RBNZ hiking to 2.50% and Fed minutes showing a divided board on further tightening suggest the global rate picture is far from settled, while domestically the ASX rotation into financials and defensives and away from resources reflects a market repositioning for a more uncertain second half. Reporting season beginning this week adds another layer of focus, with earnings quality likely to matter more than macro momentum in the near term.

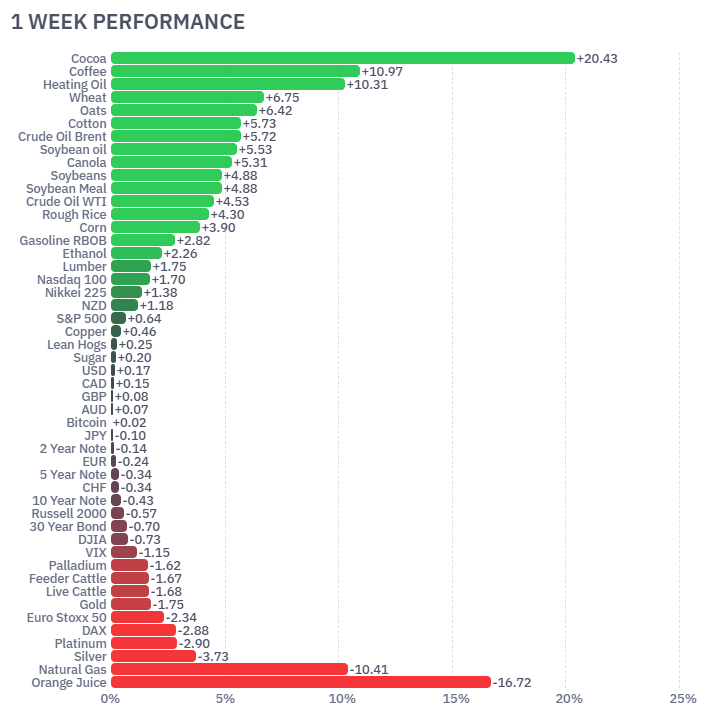

Futures Market Performance

Commodity markets dominated performance this week as geopolitical tensions following Iran’s renewed disruption of shipping through the Strait of Hormuz lifted energy markets. Heating oil rose (+8.6%), WTI crude gained (6.3%) and Brent crude climbed (+5.5%) on supply concerns. Agricultural commodities also rallied strongly, with cocoa surging (+20.2%), coffee up (+11.1%) and corn rising (+7.5%) as traders priced in adverse weather, El Niño risks and tightening global inventories. In contrast, natural gas fell (-10.3%) as milder weather reduced demand. US equity futures were firmer, led by the Nasdaq (+0.7%) and S&P 500 (+0.5%), while bond yields eased modestly and the Australian dollar finished with little change.

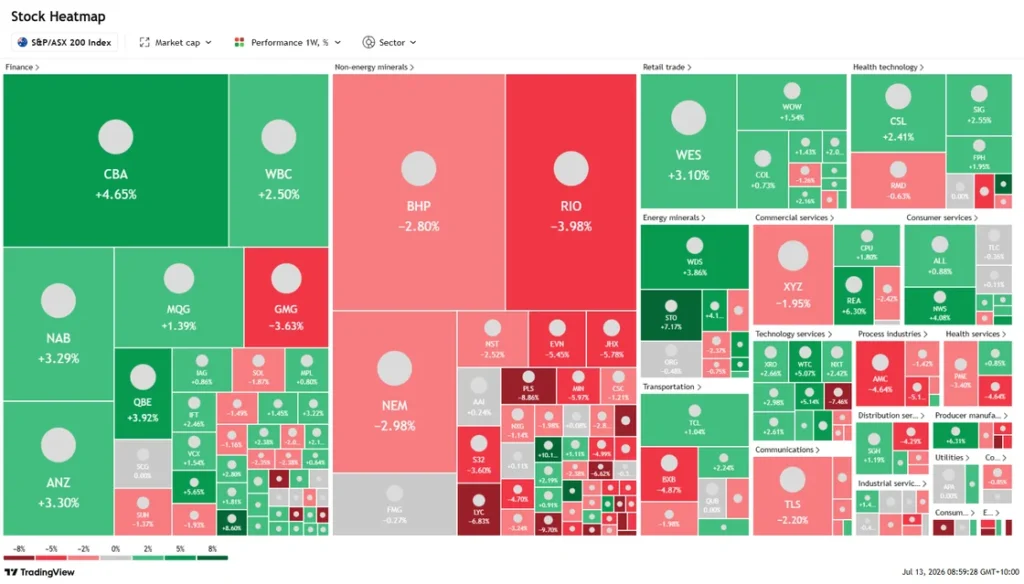

ASX Weekly Heatmap

The Australian market delivered a mixed performance. Financials provided the strongest support, with CBA gaining (+4.70%), while NAB(+3.29%), ANZ (+3.30%) and Westpac (+2.50%) also posted solid advances as investors rotated into defensive earnings. Retailers, healthcare and technology generally finished higher, led by Wesfarmers(+3.10%) and CSL(+2.41%). The major drag came from the resources sector, where BHP(-2.80%), Rio Tinto(-3.98%), Fortescue(-0.27%) and gold miners declined on softer metal prices and ongoing concerns around Chinese demand, offsetting strength across much of the broader market.

If any of this week’s developments raise questions about your portfolio, please get in touch.

Related Insights

US payrolls missed sharply at 57K this week, lifting rate cut expectations and supporting a broadly...

The RBA held the cash rate steady at 4.35% this week, supporting Australian equities while the Bank...

The US Iran peace deal dominated global markets this week, rapidly unwinding geopolitical risk premi...