A global markets summary, for

Australian investors

The US Iran peace deal dominated global markets this week, rapidly unwinding geopolitical risk premiums built up over months of conflict and driving one of the sharpest single-week moves in energy markets seen this year.

Five key developments:

1. US and Iran complete Peace deal to cease all military operations

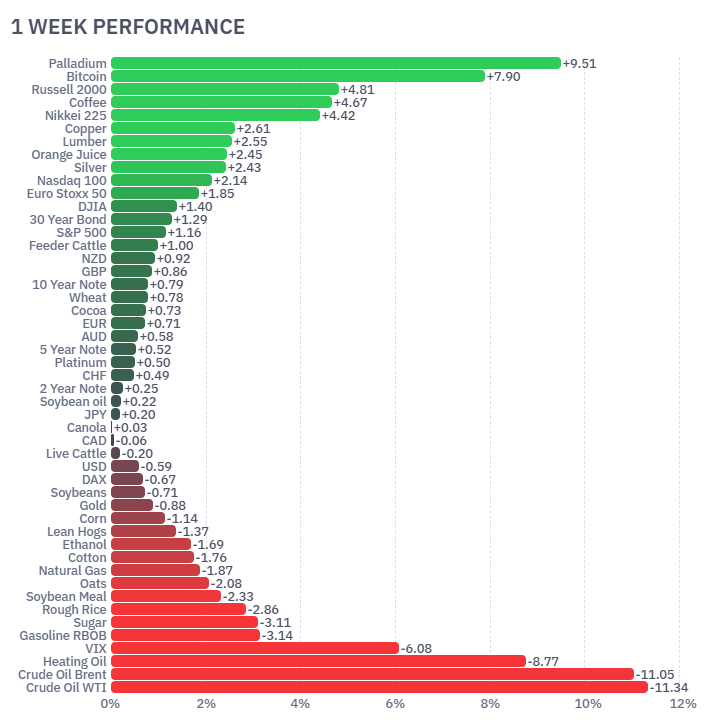

Markets responded very positively to the announcement of a peace agreement between the US and Iran, with geopolitical risk premiums rapidly unwinding across global markets. Energy markets saw the sharpest reaction, with Crude Oil WTI falling -11.34% and Brent declining -11.05% for the week. The easing geopolitical backdrop also drove a sharp compression in volatility, with the VIX falling -6.08%, while higher beta assets including small caps and crypto rallied strongly.

2. US Core CPI steady at 2.9% y/y

US Core CPI came in broadly in line with expectations at 2.9%, reinforcing the view that inflation continues to gradually moderate. Combined with the sharp decline in oil prices throughout the week, markets interpreted the result positively and continued pricing in a more supportive backdrop for risk assets. US equities rallied strongly, led by the Nasdaq 100 (+2.14%) and Russell 2000 (+4.81%), while bond markets also strengthened modestly.

3. European Central Bank raises interest rates to 2.4%

The ECB raised rates to 2.4% during the week, maintaining a relatively cautious stance toward inflation despite slowing growth across parts of Europe. European equities remained resilient following the decision, with the Euro Stoxx 50 rising +1.85%. Markets increasingly appear to believe that developed market central banks are approaching terminal rates, although policymakers remain reluctant to signal any aggressive easing cycle near term.

4. US Core PPI lower than expectations at 0.4%

US Core PPI came in below expectations at 0.4%, further supporting the broader disinflation narrative. Softer producer inflation helped support growth-oriented sectors globally, particularly technology and healthcare. Lower upstream pricing pressures are also constructive for corporate margins moving forward, with markets continuing to favour longer-duration growth assets following the result.

5. Bank of Canada holds rates steady at 2.25%

The Bank of Canada left interest rates unchanged at 2.25%, reflecting a more balanced approach as inflation moderates and growth expectations stabilise. Currency markets were relatively subdued overall, although the USD weakened modestly throughout the week while risk-sensitive currencies including the AUD and NZD strengthened. The broader macro backdrop remains supportive for risk assets in the short term as volatility declines and inflation pressures continue easing.

Australian Focus

Australian GDP growing at just 0.3% against expectations of 0.9% was the standout domestic data point this week, confirming that higher interest rates are weighing materially on household demand and broader economic activity. The weak print reduces the case for further RBA tightening but does little to resolve the inflation challenge in the near term.

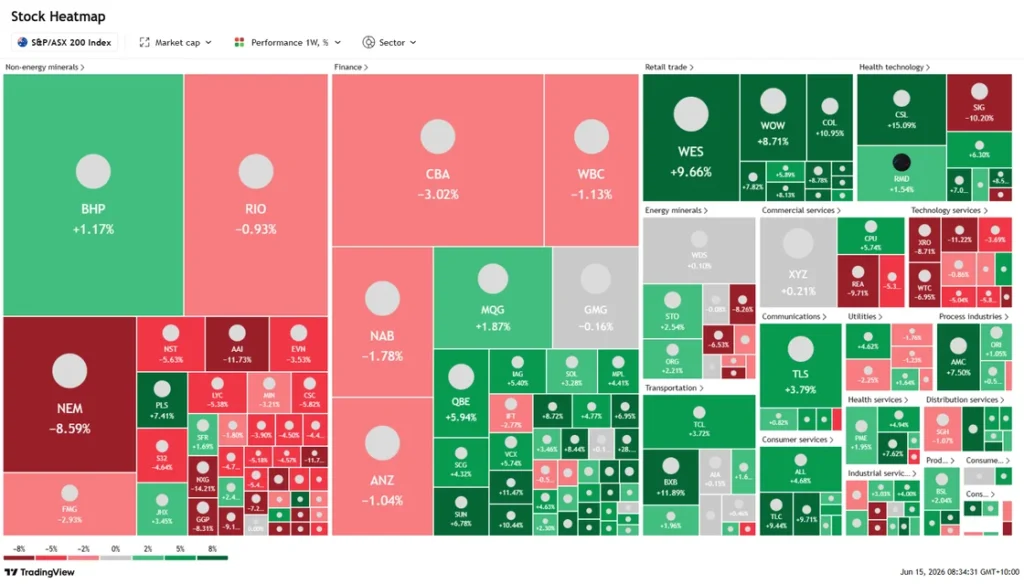

For Australian investors, the combination of soft Australian GDP and US employment running well above expectations creates a difficult cross-current. Rising US bond yields driven by the strong payrolls result pressured resources, banks, and growth stocks simultaneously, as visible in the ASX heatmap. Defensives and high-quality earnings names held up better, and that rotation is likely to continue while domestic growth stays soft and global rate expectations stay elevated.

Futures Market Performance

The dominant move this week was the aggressive unwind across energy markets following the US-Iran peace agreement. Crude Oil WTI (-11.34%), Brent (-11.05%) and Heating Oil (-8.77%) all saw heavy selling pressure as geopolitical risk premiums rapidly disappeared from the market. Risk assets broadly rallied, with strong gains across Bitcoin (+7.90%), Russell 2000 (+4.81%), Nikkei 225 (+4.42%) and Palladium (+9.51%), while volatility compressed sharply with the VIX down (-6.08%).

ASX Weekly Heatmap

The ASX 200 showed strong sector divergence throughout the week, with technology, healthcare and consumer discretionary stocks materially outperforming. CSL (+15.09%), Technology One (+11.89%), WiseTech (+7.50%) and Wesfarmers (+9.66%) were among the strongest performers. Weakness was concentrated in energy, gold and large-cap mining names following the sharp decline in commodity prices, while the major banks also lagged overall, with CBA (-3.02%), NAB (-1.78%) and ANZ (-1.04%) weighing on broader index performance.

If any of this week’s developments raise questions about your portfolio, please get in touch.

Related Insights

Australian GDP growth disappointed sharply this week at 0.3% against expectations of 0.9%, while US...

Australian CPI inflation rose 0.4% m/m this week, missing expectations and reinforcing the higher-fo...

The Strait of Hormuz reopening eased geopolitical risk premiums this week as Australian unemployment...