A global markets summary,

for Australian investors

The RBA interest rate rise to 3.85% this week extended mortgage pressure on Australian households, as US manufacturing returned to expansion and labour markets in New Zealand and the US showed early signs of cooling.

Five key developments:

1. US ISM Manufacturing PMI expands to 52.6 vs 48.5 expected

US manufacturing returned firmly to expansion territory, signalling improving industrial momentum and suggesting demand conditions are stabilising after a softer period. The upside surprise points to better inventory cycles and potential capital expenditure support, reinforcing confidence in the growth backdrop while reducing the likelihood of near-term aggressive policy easing as the outlook tilts modestly pro-growth.

2. RBA raises interest rates to 3.85%

The RBA delivered a further rate hike, underscoring its commitment to returning inflation to target amid still-resilient domestic demand. Higher borrowing costs are expected to weigh gradually on consumption and housing activity, but the move reinforces policy credibility and inflation discipline, suggesting rates may remain restrictive for longer as the outlook shifts toward controlled economic moderation.

3. NZ unemployment change rises 0.5% q/q

New Zealand’s unemployment increase signals emerging softness in labour conditions as prior tightening flows through the economy. Cooling employment typically dampens wage pressure and supports disinflation, giving the central bank greater flexibility over time, while the data points to slowing growth dynamics as the outlook becomes incrementally more cautious.

4. US JOLTS job openings contract to 6.54M vs 7.25M expected

Job openings fell more than anticipated, indicating labour demand is easing and that rebalancing is underway. While still above pre-pandemic norms, the decline suggests firms are becoming more measured in hiring plans, helping reduce wage-driven inflation risks and supporting the case for policy patience as the outlook trends toward a softer but stable labour market.

5. Bank of England leave interest rates unchanged at 3.75%

The Bank of England held rates steady, signalling policymakers prefer to assess prior tightening before adjusting settings further. Sticky services inflation remains a concern, but holding steady balances growth risks against price stability objectives, reinforcing expectations for a prolonged plateau in policy rates as the outlook favours cautious stability.

Australian Focus

The RBA interest rate rise to 3.85% was the defining domestic development this week, but the broader picture added important context. US manufacturing returning firmly to expansion and job openings contracting sharply together paint a picture of an economy slowing in the right places, while the Bank of England holding steady reinforced the global trend of central banks pausing to assess prior tightening.

For Australian investors, the RBA interest rate rise extends mortgage pressure and keeps rate-sensitive sectors challenged, while cooling US labour demand and New Zealand unemployment rising suggest global disinflation is progressing in a way that eventually supports the case for an RBA pause. Resources face near-term headwinds given softer demand signals, but financials with pricing power and defensives remain better placed as conditions moderate.

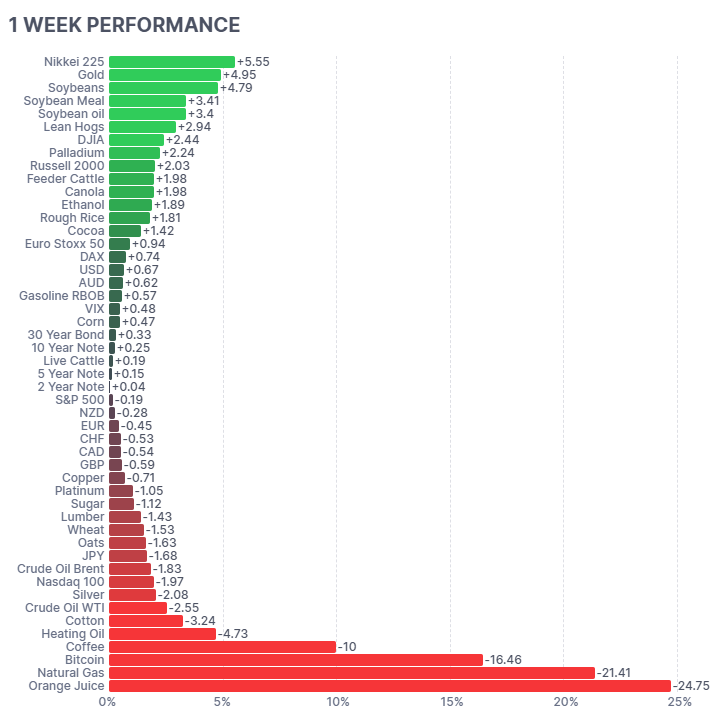

Futures Market Performance

Futures markets showed a clear risk-off rotation beneath the surface despite pockets of strength. Defensive metals rallied, with Gold (+4.95%) benefiting from rate uncertainty, while the Nikkei 225 (+5.55%) led global equity futures higher on improving growth sentiment. Agricultural markets were mixed, with Soybeans (+4.79%) advancing but Orange Juice (-24.75%) and Natural Gas (-21.41%) collapsing on supply dynamics. Crypto also saw heavy pressure, with Bitcoin (-16.46%) and Coffee (-10.00%) sharply lower, while crude softened (WTI -2.55%), pointing to demand concerns and elevated volatility (VIX +0.48%).

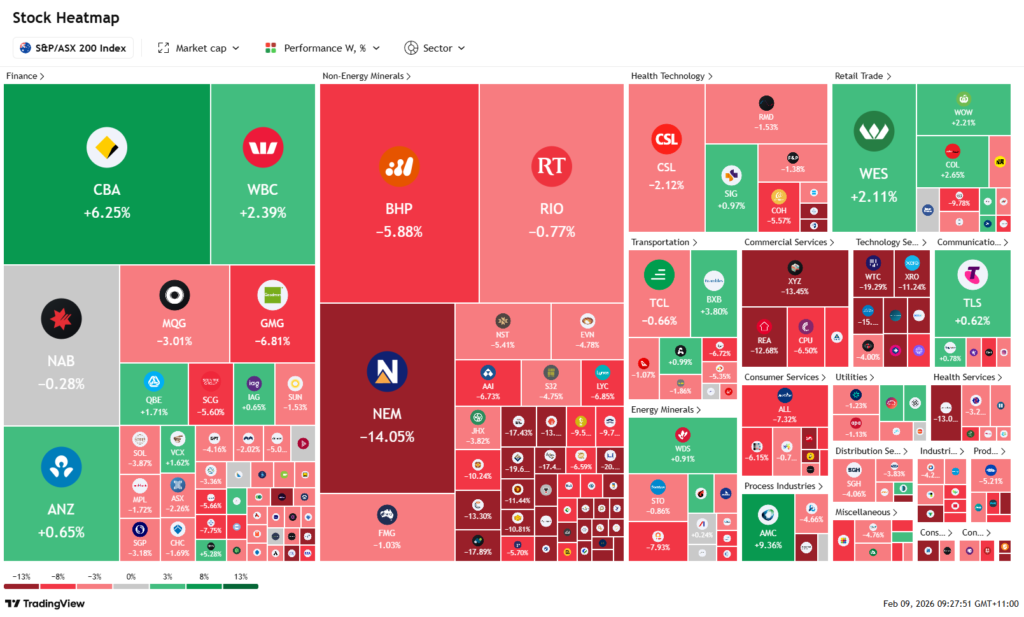

ASX Weekly Heatmap

The ASX experienced broad weakness driven primarily by heavy losses across large-cap miners. BHP (-5.88%) and NEM (-14.05%) weighed materially on the index as commodity sensitivity resurfaced, while Rio (-0.77%) also detracted. Financials were mixed but relatively resilient, with CBA (+6.25%) outperforming and WBC (+2.39%) higher, offsetting declines in MQG (-3.01%). Technology and growth names sold off aggressively, including WTC (-19.29%) and XRO (-11.24%), highlighting a sharp rotation toward defensives as volatility increased and investors reduced cyclically exposed positions.

If any of this week’s developments raise questions about your portfolio, please get in touch.

Related Insights

Iran's renewed blockade of the Strait of Hormuz reignited energy supply concerns this week, pushing...

US payrolls missed sharply at 57K this week, lifting rate cut expectations and supporting a broadly...

The RBA held the cash rate steady at 4.35% this week, supporting Australian equities while the Bank...