A global markets summary, for

Australian investors

Five key developments:

1. NZ CPI increases to 0.9% m/m vs 0.6% previous

New Zealand inflation re-accelerated, with quarterly CPI rising to 0.9%, above both the prior 0.6% and market expectations near 0.8%. Annual inflation held around 3.1%, keeping price pressures above the RBNZ’s comfort zone. The stronger non-tradables component suggests domestic inflation remains sticky, leaving the outlook tilted toward a slower easing cycle.

2. US Core Retail Sales m/m rise to 1.9%

US retail spending strengthened sharply, with underlying sales measures showing consumers remain resilient despite higher energy prices and tighter financial conditions. The data supports the view that household demand has not rolled over, reducing near-term recession concerns. The outlook is constructive for growth, but persistent demand may keep inflation risks elevated.

3. European PMI’s broadly rise

European PMI data broadly improved, signaling a modest recovery in business activity across services and manufacturing. The improvement suggests the region is stabilising after a weaker growth patch, helped by firmer demand and easing financial stress. The outlook is cautiously positive, though higher oil prices remain a key risk to margins and consumer confidence.

4. US/Iran back and forth continues

US-Iran tensions remained the dominant macro risk, with stalled talks and disruptions around the Strait of Hormuz driving oil sharply higher. Brent crude traded above US$100, with reports of further supply-chain pressure and energy-market repricing. The outlook remains highly sensitive to diplomatic progress, with inflation expectations likely to rise if energy prices stay elevated.

5. British Retail Sales m/m 0.7% vs -0.6% previous

British retail sales rebounded to 0.7% after the prior -0.6% decline, pointing to a firmer consumer backdrop. The data suggests spending momentum improved despite political uncertainty and broader cost-of-living pressure. The outlook is mildly supportive for UK growth, though elevated energy prices and cautious Bank of England policy remain headwinds.

Australian Focus

US consumers held firm with retail sales surging to 1.9%, European PMIs stabilised, and UK spending rebounded — but all of it is increasingly secondary to Brent crude trading above $100 as US-Iran tensions keep energy markets in repricing mode.

For Australian investors, elevated oil prices feed directly into domestic inflation and RBA caution, with any diplomatic breakthrough the key swing factor. Energy exposure remains the core tactical position while rate-sensitive and consumer-facing sectors stay under pressure.

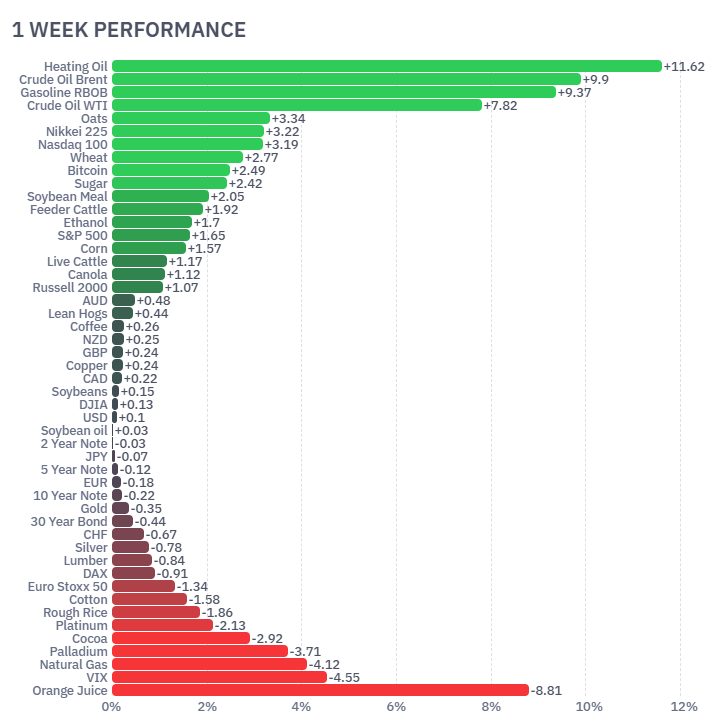

Futures Market Performance

Futures were led by a sharp energy rally, with Heating Oil (+11.62%), Brent Crude (+9.90%), RBOB Gasoline (+9.37%) and WTI Crude (+7.82%) surging as US-Iran tensions and Strait of Hormuz disruption risks tightened supply expectations. Equity futures were firmer, including Nasdaq 100 (+3.19%) and S&P 500 (+1.65%), while volatility fell as VIX dropped (-4.55%). Soft commodities were mixed, with Orange Juice (-8.81%), Cotton (-1.58%) and Rough Rice (-1.86%) weaker. Natural Gas (-4.12%) also fell, diverging from the oil complex.

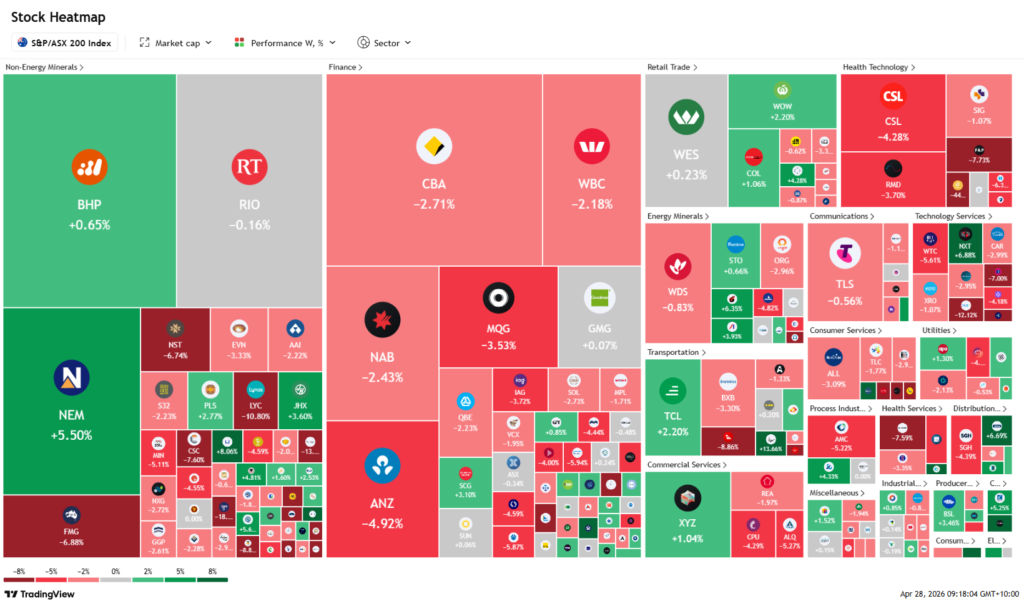

ASX Weekly Heatmap

The ASX was mixed, with miners outperforming while banks and healthcare weighed. Newmont (+5.50%) and BHP (+0.65%) supported materials as gold and hard-asset demand remained firm, while Rio Tinto (-0.16%) was flat. Financials were broadly weaker, led by ANZ (-4.92%), Macquarie (-3.53%), CBA (-2.71%), NAB (-2.43%) and Westpac (-2.18%). Healthcare also dragged, with CSL (-4.28%) and ResMed (-3.70%) lower. Energy was mixed despite the oil rally, with Woodside (-0.83%) down and Santos (+0.66%) slightly higher.

If any of this week’s developments raise questions about your portfolio, please get in touch.

Related Insights

Iran's renewed blockade of the Strait of Hormuz reignited energy supply concerns this week, pushing...

US payrolls missed sharply at 57K this week, lifting rate cut expectations and supporting a broadly...

The RBA held the cash rate steady at 4.35% this week, supporting Australian equities while the Bank...