A global markets summary, for

Australian investors

Five key developments:

1. US strikes Iran, killing Iranian leader

The US-Israeli strike that killed Iran’s supreme leader marks one of the most significant geopolitical escalations in decades, raising the risk of regional conflict and retaliation across the Middle East. Markets immediately repriced energy security and safe-haven demand, and sustained uncertainty is likely to keep volatility elevated and risk sentiment fragile as the outlook shifts toward geopolitical-driven market moves.

2. Australian m/m CPI rises 0.4% vs 0.2% expected

Australian inflation surprised to the upside, reinforcing concerns that domestic price pressures remain sticky despite restrictive policy settings. Stronger housing and services costs continue to underpin inflation persistence, reducing the likelihood of near-term easing and keeping the RBA biased toward a tighter stance as the outlook for rates remains higher for longer.

3. US unemployment claims steady at 212K vs 217K expected

US jobless claims remained stable and below expectations, highlighting continued resilience in the labour market. Ongoing employment strength supports consumption and economic stability but also limits the urgency for aggressive policy easing, reinforcing expectations that rates will remain restrictive while inflation progress is monitored as the outlook stays balanced.

4. US core PMI m/m rises 0.8% vs 0.3% expected

The stronger PMI reading points to improving underlying business activity and suggests the US economy continues to expand despite higher rates. Firm services and manufacturing momentum supports growth expectations and reduces recession risk, allowing policymakers to remain patient while monitoring inflation dynamics as the outlook tilts modestly pro-growth.

5. NZ retail sales q/q rise 0.9% vs 0.6% expected

New Zealand retail sales exceeded expectations, signalling improving consumer demand and stabilising economic momentum after a softer period. Stronger spending reduces downside growth risks and supports business confidence, potentially giving policymakers more flexibility to remain patient on further easing as the outlook shows gradual improvement.

Australian Focus

The US-Israeli strike killing Iran’s supreme leader dominated the week, immediately repricing energy risk and safe-haven demand while resilient US labour markets and a strong PMI print held the growth narrative intact.

For Australian investors, the hotter domestic CPI at 0.4% m/m removes any near-term RBA easing prospect. Combined with elevated Hormuz risk pushing energy costs higher, the setup favours domestic energy exposure and defensives over rate-sensitive growth stocks.

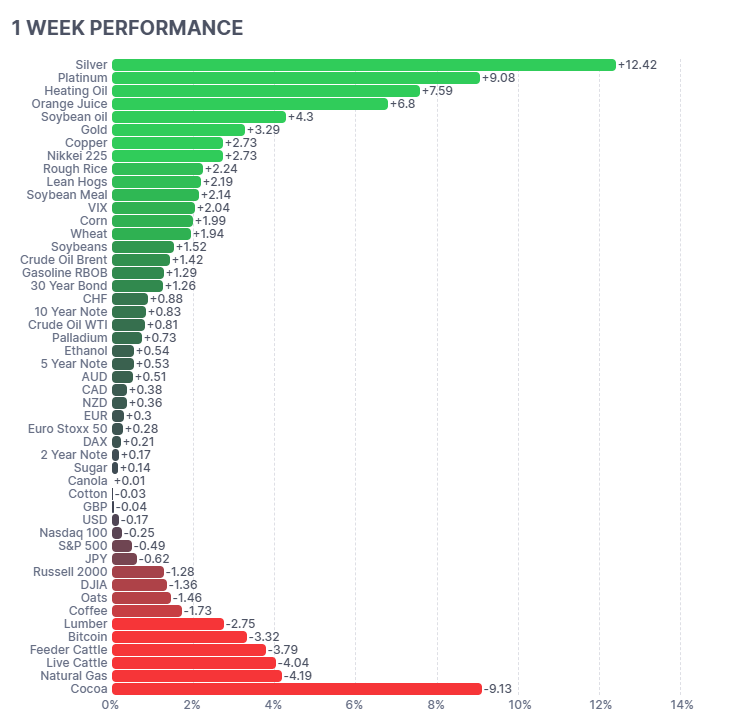

Futures Market Performance

Futures markets were dominated by a sharp volatility and commodity-led rally. Precious metals surged with Silver (+12.42%) and Platinum (+9.08%), reflecting safe-haven demand following geopolitical escalation, while Heating Oil (+7.59%) and Orange Juice (+6.80%) led broader commodity strength. Energy volatility remained elevated with Natural Gas (-4.19%) and Cocoa (-9.13%) weaker on supply dynamics. Equity sentiment softened modestly with the S&P 500 (-0.49%) and Nasdaq (-0.25%) drifting lower as volatility rose (VIX +2.04%) amid heightened geopolitical risk.

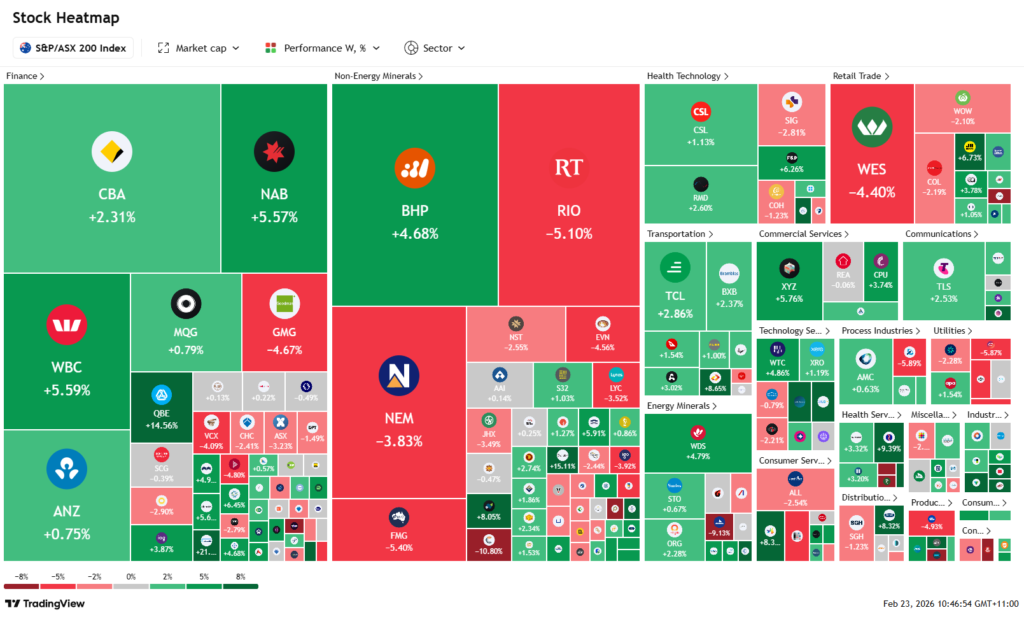

ASX Weekly Heatmap

The ASX delivered a strong week driven by a powerful rally in resources and financials. BHP (+10.21%), RIO (+1.41%) and NEM (+9.11%) led gains as investors rotated into commodities and defensives, while banks were mixed with NAB (+1.76%) and WBC (+1.55%) offsetting weakness in CBA (-1.90%) and MQG (-3.64%). Technology and growth names remained under pressure, including CSL (-3.80%) and WES (-5.69%), highlighting a continued rotation toward cyclicals and hard assets.

If any of this week’s developments raise questions about your portfolio, please get in touch.

Related Insights

Iran's renewed blockade of the Strait of Hormuz reignited energy supply concerns this week, pushing...

US payrolls missed sharply at 57K this week, lifting rate cut expectations and supporting a broadly...

The RBA held the cash rate steady at 4.35% this week, supporting Australian equities while the Bank...