A global markets summary, for

Australian investors

“Iran conflict oil prices dominated global markets this week, with US-Israeli operations against Iranian assets pushing Brent and WTI sharply higher as Hormuz disruption risk kept inflation expectations elevated across developed economies.

Five key developments:

1. US/Israel/Iran conflict continues – with no end in sight

Geopolitical tensions remain elevated as the United States and Israel continue military operations targeting Iranian assets while Iran has retaliated with missile and drone strikes across the region. Energy markets have reacted sharply, with oil prices surging and shipping risks rising around the Strait of Hormuz. The conflict is increasingly shaping global macro sentiment, reinforcing inflation risks and keeping markets cautious toward risk assets.

2. Chinese CPI y/y rises 1.3% vs 0.9% expected

China’s inflation surprised to the upside with CPI rising 1.3% year-on-year, beating expectations of 0.9% and marking the strongest reading in several years as holiday spending and services demand lifted prices. Despite the stronger print, underlying economic momentum remains uneven due to property market weakness and subdued domestic demand, suggesting policymakers may still lean toward supportive stimulus if growth softens.

3. US CPI steady at 0.2%

US inflation showed signs of stabilising with CPI holding at 0.2% month-on-month, suggesting price pressures are not accelerating dramatically despite geopolitical shocks. Markets interpreted the data as consistent with a “higher for longer” interest-rate environment rather than immediate tightening, with investors continuing to watch energy prices closely as the Iran conflict threatens to feed through to headline inflation.

4. British GDP m/m shows no growth

The UK economy stalled over the latest month with GDP registering zero growth, highlighting the fragile nature of Britain’s recovery as higher interest rates and weak consumer demand continue to weigh on activity. The flat reading reinforces expectations that the Bank of England will remain cautious on policy easing while monitoring inflation persistence and global geopolitical developments.

5. US Core PCE Price Index m/m steady at 0.4%

The Federal Reserve’s preferred inflation gauge, core PCE, rose 0.4% month-on-month, exceeding expectations and reinforcing concerns that underlying inflation remains sticky. The data suggests price pressures in services and discretionary sectors continue to run above the Fed’s 2% target, complicating the central bank’s ability to cut rates in the near term.

Australian Focus

Iran conflict oil prices dominated the macro backdrop for a third consecutive week, keeping energy markets elevated and global risk sentiment cautious as Hormuz disruption fears continued feeding through to inflation expectations worldwide.

For Australian investors, sticky US core PCE, a Chinese inflation beat, and flat UK growth combine to paint a stagflationary picture that keeps the RBA on hold. Energy and resources remain the tactical allocation, while rate-sensitive and consumer-facing sectors stay under pressure.

Futures Market Performance

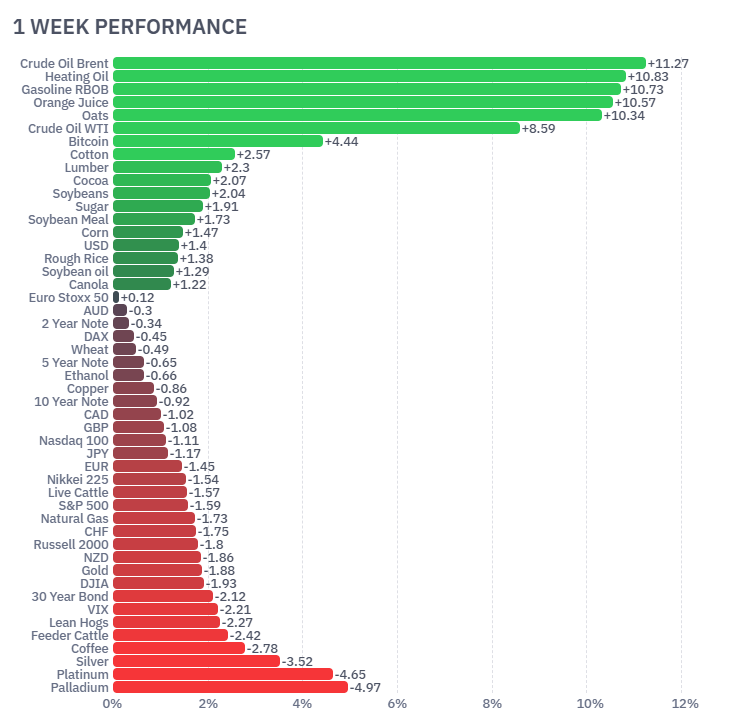

Commodity markets were dominated by energy and agricultural strength as geopolitical risk drove a sharp rally in oil. Brent crude (+11.27%), heating oil (+10.83%), gasoline RBOB (+10.73%) and WTI crude (+8.59%) surged on concerns about supply disruptions through the Strait of Hormuz. Agricultural commodities also firmed, with orange juice (+10.57%), oats (+10.34%), soybean oil (+1.29%), corn (+1.47%) and sugar (+1.91%) moving higher as inflation hedging and weather concerns supported prices. In contrast, risk assets struggled with the S&P 500 (-1.59%), Nasdaq (-1.11%) and Russell 2000 (-1.83%) declining while precious metals diverged with gold (-1.88%), platinum (-4.65%) and palladium (-4.97%) weakening.

If any of this week’s developments raise questions about your portfolio, please get in touch.

Related Insights

Iran's renewed blockade of the Strait of Hormuz reignited energy supply concerns this week, pushing...

US payrolls missed sharply at 57K this week, lifting rate cut expectations and supporting a broadly...

The RBA held the cash rate steady at 4.35% this week, supporting Australian equities while the Bank...