A global markets summary, for

Australian investors

Central bank policy Australia and across developed markets held steady this week, with flat Canadian inflation, the RBNZ pausing at 2.25%, and stable domestic wage growth reinforcing a restrictive-but-stable policy plateau.

Five key developments:

1. Canadian CPI flat at 0.0%

Canada’s latest CPI print came in flat at 0.0%, reinforcing the view that inflationary pressures across developed markets are continuing to stabilise after an extended tightening cycle. While disinflation has largely played out, the absence of renewed price pressures gives the Bank of Canada flexibility to maintain its current policy stance. With global growth showing resilience but not overheating, markets are increasingly comfortable with a prolonged period of stable rates and steady policy settings across North America.

2. RBNZ holds cash rate steady at 2.25%

The Reserve Bank of New Zealand kept its cash rate unchanged at 2.25%, signalling confidence that current policy remains sufficiently restrictive to contain inflation without further tightening. Forward guidance suggests a data-dependent approach, with policymakers watching labour market and housing indicators closely. Stability from the RBNZ adds to the broader global narrative of central banks pausing rate adjustments, which supports risk sentiment and reinforces expectations that policy rates are near their cyclical peak across developed markets.

3. Australian wage price index steady at 0.8% q/q

Australia’s wage price index held steady at 0.8% q/q, indicating continued but controlled wage growth across the domestic economy. While still elevated compared to pre-pandemic norms, the data suggests wage pressures are not accelerating further, providing the RBA with breathing room to assess broader inflation dynamics. A stable wage environment supports consumer spending without reigniting inflation concerns, reinforcing expectations that monetary policy will remain relatively steady as policymakers balance growth and price stability.

4. US core durable goods rise to 0.9% m/m

US core durable goods orders surprised to the upside, rising 0.9% m/m and highlighting ongoing resilience in business investment and manufacturing demand. The strength suggests corporate confidence remains intact despite higher borrowing costs and lingering geopolitical risks. Continued capital expenditure supports the broader US growth outlook and reinforces the narrative of economic durability. With activity indicators remaining firm, markets continue to expect steady growth rather than a sharp slowdown across the US economy.

5. Australian unemployment change 17.8K vs 68.5K previous

Australian employment rose by 17.8K, down from the previous 68.5K increase but still reflective of a labour market that remains structurally tight. While the pace of job creation has moderated, underlying demand for labour continues to support incomes and consumption. The moderation helps alleviate pressure on wages and inflation, allowing the RBA to maintain a balanced stance. Overall, the labour market remains supportive of economic stability, with no immediate signs of deterioration in domestic conditions.

Australian Focus

Central banks across developed markets held steady this week, with flat Canadian inflation, the RBNZ pausing at 2.25%, and stable Australian wage growth reinforcing the view that policy settings have reached a restrictive but stable level after an extended tightening cycle.

For Australian investors, this global policy plateau alongside resilient US capital expenditure and a moderating but still tight domestic labour market supports expectations for steady RBA settings and favours quality cyclicals over rate-sensitive growth stocks as conditions stabilise without overheating.

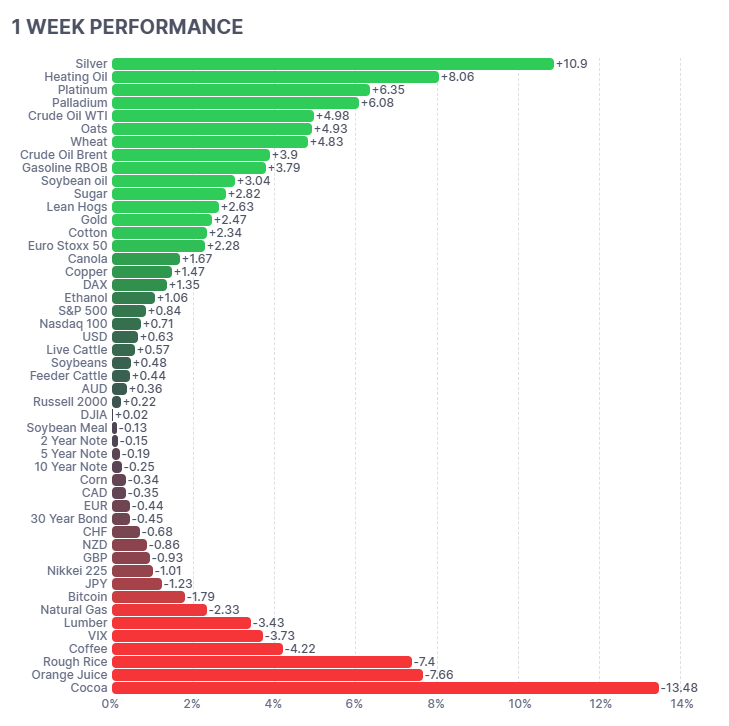

Futures Market Performance

Commodity markets were broadly strong over the week, led by precious metals and energy. Silver surged (+10.9%), heating oil rallied (+8.06%) and platinum (+6.35%) and palladium (+6.08%) posted strong gains as inflation-hedging and industrial demand returned. Crude oil WTI (+4.98%) and key agricultural contracts including wheat (+4.83%) and oats (+4.93%) also moved higher. Equity indices were steady with the S&P 500 (+0.84%) and Nasdaq (+0.71%) edging up, while the USD (+0.63%) firmed modestly. Weakness appeared in softs and select commodities, with cocoa (-13.48%), orange juice (-7.66%), rough rice (-7.4%) and coffee (-4.22%) sharply lower, reflecting positioning adjustments and easing supply concerns.

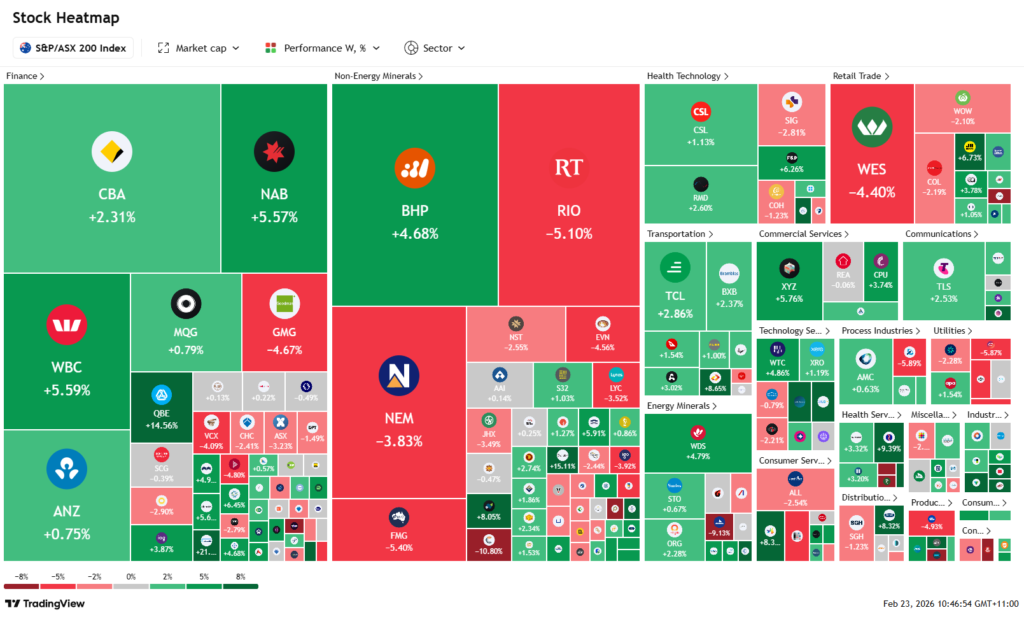

ASX Weekly Heatmap

The Australian market finished the week mixed with strong rotation beneath the surface. Financials led higher as NAB (+5.57%), Westpac (+5.59%) and CBA (+2.31%) rallied, while ANZ (+0.75%) lagged slightly but remained positive. Resource stocks diverged, with BHP (+4.68%) and Woodside (+4.79%) stronger, offset by sharp falls in Rio Tinto (-5.10%) and Fortescue (-5.40%). Gold names were softer with Newmont (-3.83%). Defensive and industrial names held firm, including Telstra (+2.53%) and Transurban (+2.86%), while retail lagged with Wesfarmers (-4.40%). Overall performance reflected sector rotation rather than broad-based weakness, with investors selectively positioning across banks, energy and defensives.

If any of this week’s developments raise questions about your portfolio, please get in touch.

Related Insights

Iran's renewed blockade of the Strait of Hormuz reignited energy supply concerns this week, pushing...

US payrolls missed sharply at 57K this week, lifting rate cut expectations and supporting a broadly...

The RBA held the cash rate steady at 4.35% this week, supporting Australian equities while the Bank...