A global markets summary, for

Australian investors

The Australian inflation and RBA cuts outlook shifted this week as easing US headline inflation and deepening Chinese disinflationary pressure pointed toward a more supportive global policy environment heading into the months ahead.

Five key developments:

1. Chinese CPI y/y 0.2% vs 0.8% previous

Chinese inflation slowed sharply, reinforcing ongoing disinflationary pressure across the domestic economy. Weak price momentum reflects subdued consumer demand and lingering property sector softness, increasing expectations for further policy support from Beijing. Persistently low inflation keeps stimulus firmly on the table, suggesting Chinese authorities will remain growth-supportive as the outlook stays soft.

2. US Core Retail Sales m/m 0.0% vs 0.3% expected

US core retail sales stalled, pointing to moderating consumer momentum after a strong prior period. The softer-than-expected print suggests higher interest rates are beginning to weigh on discretionary spending, easing demand-driven inflation risks. Slowing consumption supports a more balanced policy path and reinforces expectations for gradual easing as the outlook becomes more mixed.

3. US average hourly earnings m/m 0.4% vs 0.1% previous

Wage growth accelerated, highlighting persistent labour market tightness and ongoing income support for households. Stronger earnings growth can sustain consumption but also risks keeping services inflation elevated. The data complicates the disinflation narrative and may keep policymakers cautious on rapid easing, maintaining a watchful stance as the outlook remains finely balanced.

4. US CPI y/y 2.4% vs 2.7% previous

Headline inflation continued to ease, reinforcing confidence that price pressures are moving toward target. The moderation supports expectations that policy settings are sufficiently restrictive, allowing central bankers greater flexibility later in the year. Continued progress on inflation strengthens the case for gradual easing while supporting risk sentiment as the outlook improves.

5. British GDP continues to slow

UK economic growth remains sluggish, reflecting ongoing pressure from higher interest rates and weak household demand. Slowing activity reduces inflationary pressure but raises downside growth risks for policymakers. With momentum softening, the Bank of England may lean toward eventual easing, supporting a cautious but stabilising outlook.

Australian Focus

The Australian inflation and RBA cuts outlook improved modestly this week as US headline inflation continued easing toward target and Chinese disinflationary pressure kept commodity demand subdued, creating a more supportive global backdrop for eventual policy relief.

For Australian investors, softening Chinese demand remains a near-term headwind for commodity exports and mining earnings, but the broader easing in global inflation supports the case for Australian inflation and RBA cuts to align over coming quarters, potentially relieving mortgage pressure and supporting domestic equities as conditions stabilise.

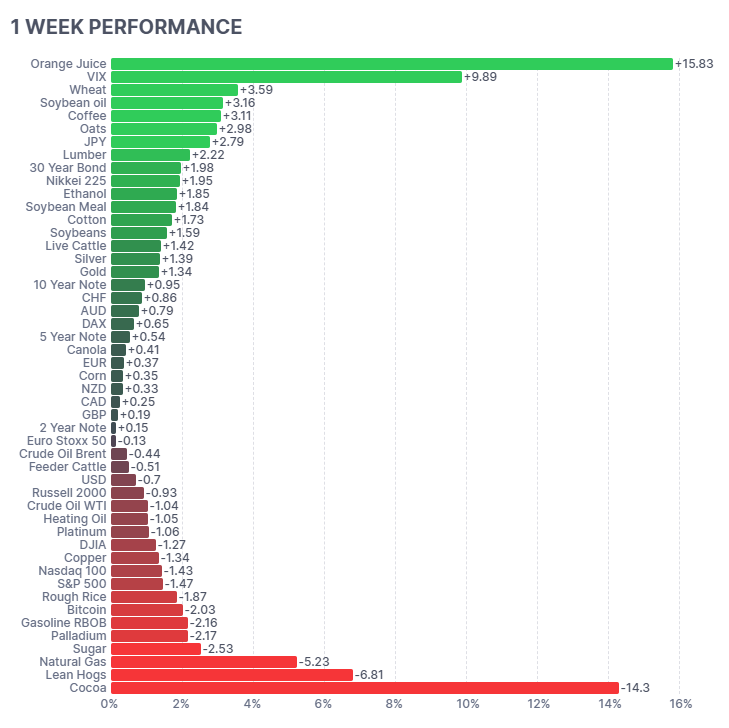

Futures Market Performance

Volatility surged across commodity markets, with sharp divergence between softs and broader risk assets. Orange Juice (+15.83%) and VIX (+9.89%) led gains, highlighting rising market uncertainty, while agricultural contracts such as Wheat (+3.59%) and Soybeans (+3.16%) were firm. Conversely, Cocoa (-14.30%), Lean Hogs (-6.81%) and Natural Gas (-5.23%) fell sharply on supply-driven pressure. Equity sentiment softened with the S&P 500 (-1.47%) and Nasdaq (-1.43%) lower, while safe-haven demand supported Gold (+1.34%) and government bonds, reinforcing a defensive market tone.

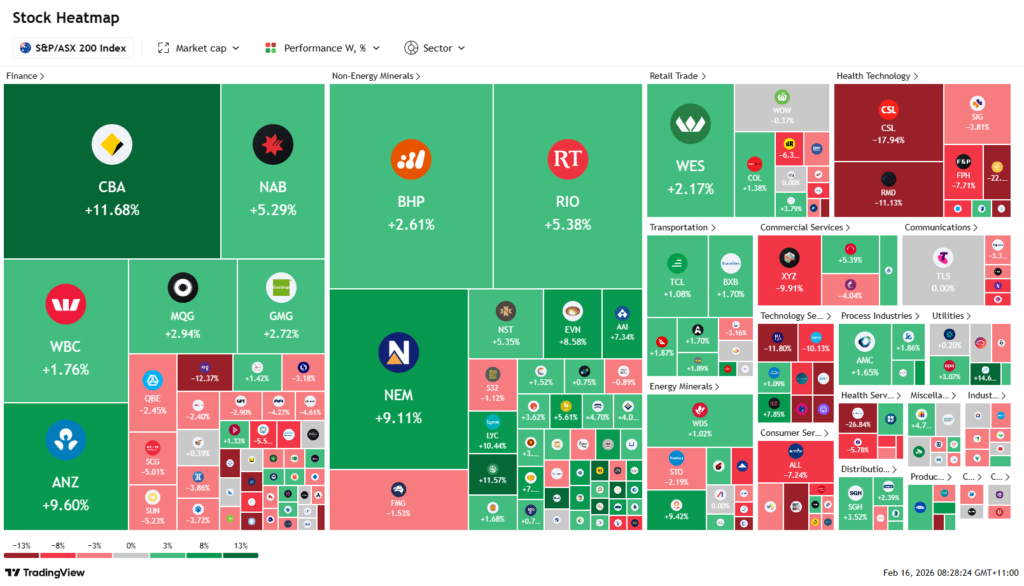

ASX Weekly Heatmap

The ASX delivered a strong week, led decisively by the major banks and large-cap miners. Financials surged with CBA (+11.68%), ANZ (+9.60%) and NAB (+5.29%) driving index performance as investors rotated into defensives. Resources were also firm, with BHP (+2.61%), RIO (+5.38%) and NEM (+9.11%) higher on stronger commodity pricing. Weakness was concentrated in healthcare and select growth names, with CSL (-17.94%) and RMD (-11.13%) dragging, highlighting sharp sector rotation beneath a strong headline index.

If any of this week’s developments raise questions about your portfolio, please get in touch.

Related Insights

Iran's renewed blockade of the Strait of Hormuz reignited energy supply concerns this week, pushing...

US payrolls missed sharply at 57K this week, lifting rate cut expectations and supporting a broadly...

The RBA held the cash rate steady at 4.35% this week, supporting Australian equities while the Bank...