A global markets summary, for

Australian investors

Five key developments:

1. US-Iran conflict escalates following targeted strike on Iranian leadership

Geopolitical tensions surged after a joint US-Israeli strike targeted senior Iranian leadership, reportedly killing Supreme Leader Ayatollah Ali Khamenei and triggering retaliatory missile and drone attacks across the Gulf region. Energy markets reacted sharply as traders priced in disruption risks to oil supply routes through the Strait of Hormuz, while investors moved toward defensive positioning amid fears of a broader regional conflict.

2. US ISM Manufacturing expands ahead of expectations

US ISM Manufacturing returned to expansion territory, surprising markets and suggesting industrial activity is stabilising after a prolonged slowdown. Stronger-than-expected new orders and production components pointed to improving demand conditions, reinforcing the view that the US economy remains resilient despite higher interest rates. The data has supported expectations that the Federal Reserve can maintain a restrictive stance without immediately threatening economic growth.

3. Australian 3-year Bond yields hit decade high

Australian short-dated bond yields pushed to their highest levels in more than a decade as investors reassessed the outlook for domestic interest rates. Persistent inflation pressures and stronger-than-expected economic data have led markets to scale back expectations for near-term rate cuts, pushing yields higher across the front end of the curve and tightening financial conditions across credit and mortgage markets.

4. Australian GDP jumps to 0.8% vs 0.5% expected

Australia’s economy expanded faster than expected, with GDP rising 0.8% for the quarter versus forecasts of 0.5%. The stronger print was driven by household consumption and public spending, suggesting domestic demand remains resilient despite elevated interest rates. The result has reinforced the view that the RBA may need to maintain restrictive policy settings for longer if inflation pressures persist.

5. US Non-farm employment change declines by -92K vs 58K expected

US non-farm payrolls surprised to the downside, with employment contracting by 92,000 compared with expectations for a 58,000 increase. The weaker labour market signal contrasts with otherwise solid economic indicators and suggests momentum in hiring may be slowing. Markets interpreted the data as an early sign that tight monetary policy is beginning to cool labour demand, tempering expectations for further aggressive rate hikes.

Australian Focus

Geopolitical escalation in the Gulf dominated the week, with the US-Israeli strike on Iranian leadership pushing energy markets sharply higher and triggering a broad defensive rotation as Hormuz supply disruption risk was priced in.

For Australian investors, the domestic picture added its own complexity: stronger-than-expected GDP and decade-high 3-year bond yields have effectively closed the door on near-term RBA cuts, while a weak US payrolls print introduces uncertainty around the global growth outlook. Energy exposure remains favoured, rate-sensitive sectors face ongoing pressure, and the GDP beat supports domestic cyclicals with pricing power.

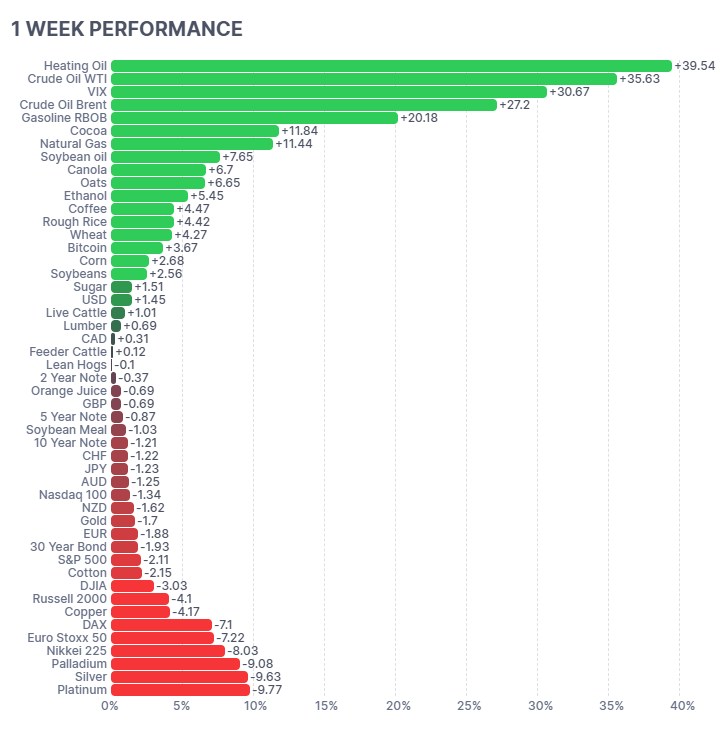

Futures Market Performance

Commodity markets were dominated by the geopolitical shock from the escalating US-Iran conflict. Energy contracts surged sharply, with Heating Oil (+39.54%), Crude Oil WTI (+35.63%) and Brent (+27.2%) leading the gains as traders priced in potential disruptions to Middle East supply routes and tanker traffic through the Strait of Hormuz. Risk hedging also lifted volatility measures, with the VIX jumping (+30.67%). Agricultural markets were broadly stronger with Cocoa (+11.84%), Natural Gas (+11.44%) and Canola (+6.7%) posting gains. In contrast, precious metals and industrial assets weakened, with Silver (-9.63%), Platinum (-9.77%) and Palladium (-9.08%) falling alongside global equity indices as risk sentiment deteriorated.

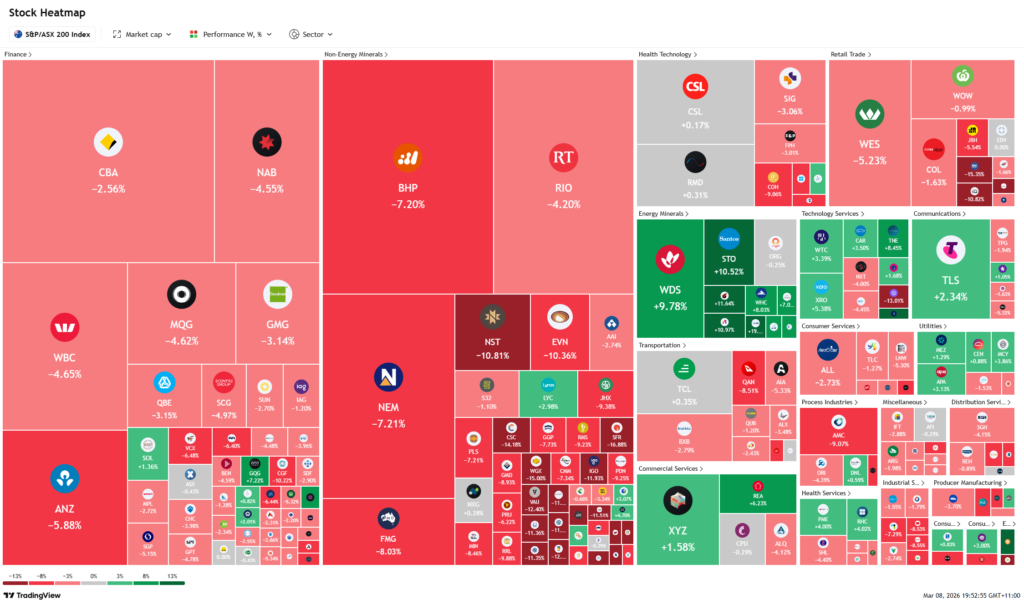

ASX Weekly Heatmap

The Australian market finished the week under heavy pressure as global risk sentiment deteriorated. The major banks were broadly weaker with CBA (-2.56%), NAB (-4.55%), WBC (-4.65%) and ANZ (-5.88%) all declining as higher bond yields weighed on valuations. The mining sector was also heavily sold, with BHP (-7.20%), Rio Tinto (-4.20%), Fortescue (-8.03%) and Newmont (-7.21%) dragging the index lower alongside gold and base metal volatility. Retail stocks were weak with Wesfarmers (-5.23%) leading declines, while energy names were the standout performers as oil prices surged, with Woodside (+9.78%) and Santos (+10.52%) rallying sharply. Defensive pockets emerged in communications, with Telstra (+2.34%) posting gains.

If any of this week’s developments raise questions about your portfolio, please get in touch.

Related Insights

Iran's renewed blockade of the Strait of Hormuz reignited energy supply concerns this week, pushing...

US payrolls missed sharply at 57K this week, lifting rate cut expectations and supporting a broadly...

The RBA held the cash rate steady at 4.35% this week, supporting Australian equities while the Bank...