A global markets summary, for

Australian investors

The Australian CPI RBA outlook remained cautious this week as flat headline inflation masked persistent core price pressures, keeping the board on hold while US-Iran diplomacy stalled without resolution.

Five key developments:

1. US & Iran have back and forth about communication

The week was dominated by conflicting signals on diplomacy. President Trump said the US had held productive exchanges with Iran and delayed threatened attacks on Iran’s power grid, while Tehran publicly denied direct negotiations were taking place. Reuters also reported that messages were still being passed through intermediaries, reinforcing that communication channels remain open even as both sides keep a hard public line, leaving markets sensitive to any shift toward either de-escalation or further conflict.

2. European PMIs mixed

Europe’s PMI picture was uneven rather than uniformly weak. Germany’s flash composite PMI slowed to 51.9 from 53.2, but manufacturing improved to 51.7, its strongest reading in 45 months, suggesting industry is stabilising. France was softer, with its composite PMI falling to 48.3 and services slipping further into contraction. The read-through is that Europe is still fragile, but not without pockets of resilience, so growth likely stays patchy while higher input costs keep pressure on margins and sentiment.

3. US Flash Manufacturing PMI expands to 52.4

US manufacturing surprised on the upside, with the S&P Global flash Manufacturing PMI rising to 52.4 in March from 51.6 in February, marking an eighth straight month of improving factory conditions. Production growth and new orders both strengthened, showing US industry is still expanding despite geopolitical turmoil and cost pressure. That keeps the US looking firmer than many developed peers for now, though rising input prices mean the market will stay alert to whether stronger activity starts feeding more stubborn inflation.

4. Australian CPI flat at 0.0% vs 0.4% previous

Australia’s monthly CPI indicator was unchanged in original terms in February after a 0.4% rise previously, while annual inflation eased to 3.7% from 3.8%. The seasonally adjusted monthly result still rose 0.2%, and trimmed mean inflation held at 3.3%, so the data was softer at the headline level without clearly resolving underlying inflation pressure. In practical terms, it gives households a brief reprieve, but it is unlikely to fully shift the RBA’s cautious stance while core price growth remains elevated.

5. US unemployment claims steady at 210k

US initial jobless claims came in at 210,000 for the week ended March 21, up 5,000 from the prior week, while the four-week average edged down to 210,500. That keeps claims near historically low levels and suggests the labour market remains broadly firm despite broader uncertainty. For markets, the result supports the view that the US economy is still holding up, meaning policymakers are unlikely to get much immediate relief from labour weakness if inflation pressures remain sticky.

Australian Focus

Australian Focus:

The Australian CPI RBA outlook remained cautious this week as flat headline inflation masked persistent core price pressures, with trimmed mean holding at 3.3% and giving the board no clear reason to shift course.

For Australian investors, the Australian CPI RBA outlook stays biased toward a prolonged hold. With the RBA already at 4.1% and US-Iran diplomacy stalling without resolution, rate-sensitive sectors remain challenged and the bias stays toward resources and defensives.

Futures Market Performance

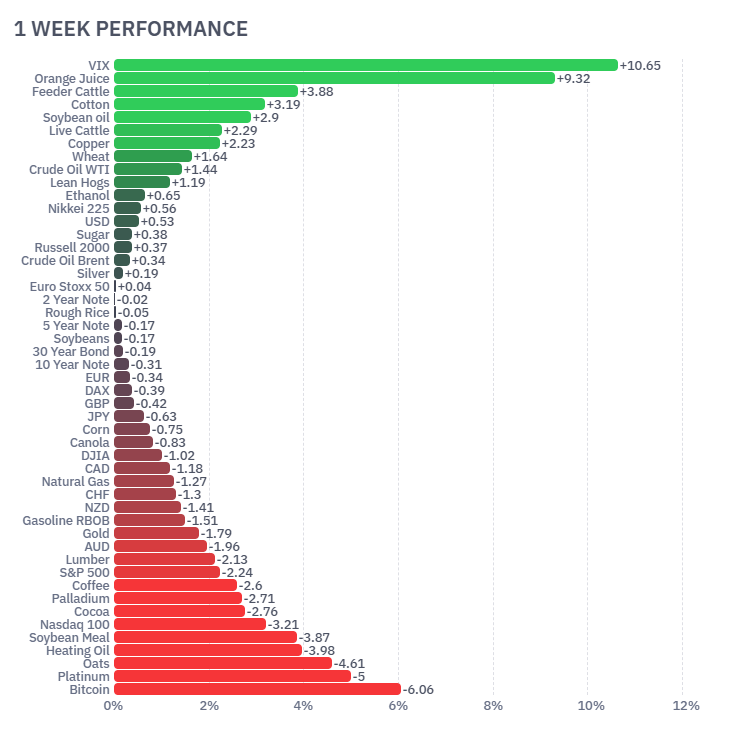

Futures markets were led by a sharp volatility spike, with VIX (+10.65%) and Orange Juice (+9.32%) topping the board, while feeder cattle (+3.88%), cotton (+3.19%), soy oil (+2.90%) and live cattle (+2.29%) also advanced. On the downside, Bitcoin (-6.06%), Platinum (-5.00%), Oats (-4.61%), Heating Oil (-3.98%), Soybean Meal (-3.87%) and Nasdaq 100 (-3.21%) were the main laggards. The mix points to rising geopolitical risk, supply-side concern and defensive positioning, with energy dislocation and war-related uncertainty lifting volatility while growth assets and crypto came under pressure.

ASX Weekly Heatmap

On the ASX, miners carried the market tone while banks were heavy. BHP (+6.74%), FMG (+6.04%), EVN (+5.59%), NEM (+5.46%), CSL (+5.29%) and RIO (+3.49%) were standout gainers, helped by stronger resource sentiment and gold-related support, while the major banks lagged badly, led by NAB (-10.55%), CBA (-2.46%), ANZ (-1.83%) and WBC (-1.02%). Tech also remained soft, with XRO (-8.01%) and WTC (-5.39%) weaker. Overall, it was a week where resources outperformed and financials dragged on the broader index.

If any of this week’s developments raise questions about your portfolio, please get in touch.

Related Insights

Iran's renewed blockade of the Strait of Hormuz reignited energy supply concerns this week, pushing...

US payrolls missed sharply at 57K this week, lifting rate cut expectations and supporting a broadly...

The RBA held the cash rate steady at 4.35% this week, supporting Australian equities while the Bank...