A global markets summary, for

Australian investors

Five key developments:

1. Bank of Japan holds rates steady at 0.75%

The Bank of Japan left rates unchanged at 0.75%, but the decision carried a hawkish edge, with three board members dissenting in favour of a hike to 1.0%. The hold reflects caution around energy-price pressure and geopolitical uncertainty, while the dissent suggests policy normalisation remains active and the outlook is for further tightening risk if inflation pressure persists.

2. Australian CPI rises to 1.1% m/m

Australian CPI rose 1.1% in March, lifting annual inflation to 4.6%, with housing, transport, and food key contributors. The fuel shock was particularly material, reinforcing household cost pressure and keeping the RBA’s inflation challenge alive. The outlook is for markets to reassess the timing of any easing, with rate-cut expectations vulnerable to further upside inflation surprises.

3. US Federal Funds Rate held at 3.75%

The Federal Reserve held the funds rate range at 3.50%–3.75%, maintaining a cautious stance as inflation remains above target while growth has not yet weakened enough to justify cuts. The decision keeps policy restrictive but flexible, and the outlook is for the Fed to remain data-dependent, with geopolitical energy shocks complicating the path toward easing.

4. US Advance GDP rises to 2.0% q/q

US advance GDP rose at a 2.0% annualised rate in Q1, rebounding from 0.5% previously, supported by investment, exports, consumer spending and government spending. The result points to a still-resilient economy, although higher imports and energy uncertainty remain headwinds, leaving the outlook constructive but vulnerable to inflation and geopolitical shocks.

5. US and Iran continue to trade misinformation

US-Iran tensions remained elevated as both sides disputed claims around shipping access, military action and control of the Strait of Hormuz. The information war added another layer of uncertainty to already fragile energy markets, keeping risk premiums elevated across oil, gas and shipping-linked assets, with the outlook dependent on whether maritime traffic can normalise without further escalation.

Australian Focus

Australian CPI surging to 1.1% m/m and annual inflation hitting 4.6% was the week’s defining domestic data point, with the fuel shock feeding directly into housing, transport, and food costs and keeping the RBA’s inflation problem firmly unresolved.

For Australian investors, any residual rate-cut expectation should now be shelved. With the Fed holding, the BOJ tilting hawkish, and Hormuz uncertainty keeping energy elevated, the environment favours energy and inflation-linked exposures while rate-sensitive sectors face a prolonged headwind.

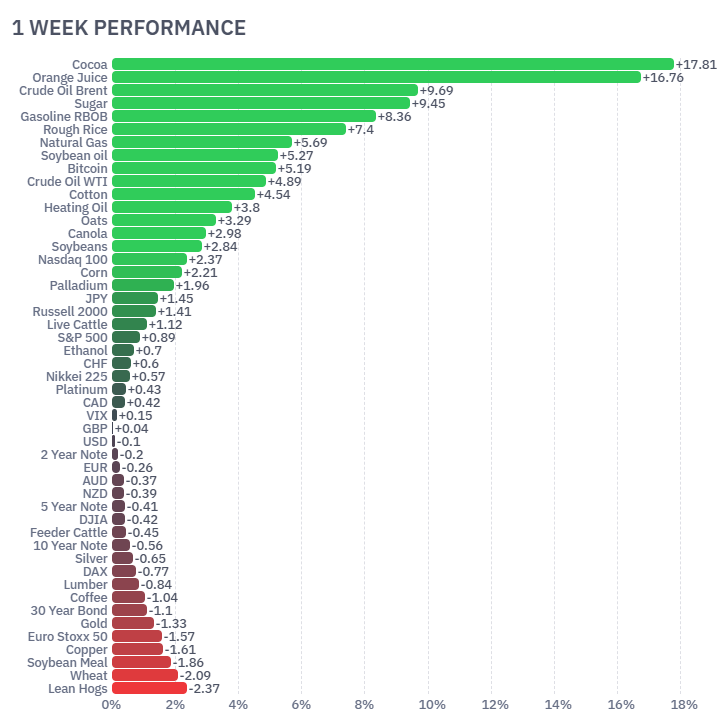

Futures Market Performance

Futures markets were led sharply higher by soft commodities, with cocoa (+17.81%), orange juice (+16.76%), crude oil Brent (+9.69%) and sugar (+9.45%) outperforming. Energy strength reflected renewed Strait of Hormuz disruption risk, while gasoline RBOB (+8.36%) and natural gas (+5.69%) also rallied on supply-risk pricing. Equity futures were firmer, led by Nasdaq 100 (+2.37%) and S&P 500 (+0.89%), while bonds weakened as inflation pressure lifted yields, with the 30 Year Bond (-1.10%) and 10 Year Note (-0.56%) lower. Metals were mixed, with gold (-1.33%) and copper (-1.61%) weaker, while wheat (-2.09%) and lean hogs (-2.37%) lagged.

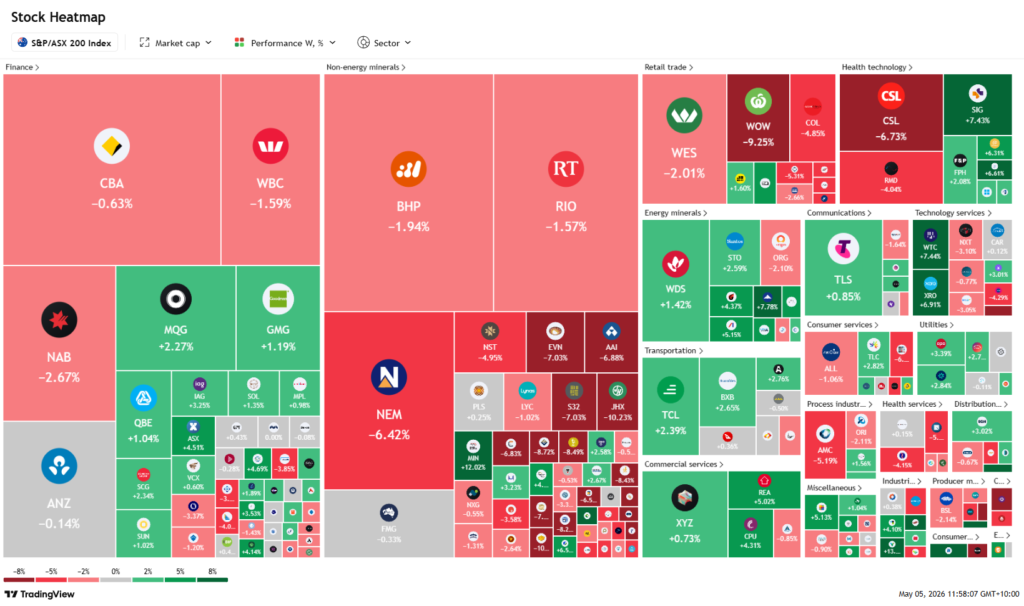

ASX Weekly Heatmap

The ASX 200 was mixed, with weakness concentrated in large-cap banks, miners and healthcare. CBA (-0.63%), WBC (-1.59%) and NAB (-2.67%) dragged the finance sector, while BHP (-1.94%), RIO (-1.57%), NEM (-6.42%) and FMG (-0.33%) weighed on resources despite strength in selected smaller miners. Healthcare was pressured by CSL (-6.73%) and RMD (-4.04%), although SIG (+7.43%) and FPH (+2.08%) offset some losses. Retail was weak, led by WOW (-9.25%) and COL (-4.85%), while strength appeared in technology and transport, including WTC (+7.44%), XRO (+6.91%) and TCL (+2.39%).

If any of this week’s developments raise questions about your portfolio, please get in touch.

Related Insights

Iran's renewed blockade of the Strait of Hormuz reignited energy supply concerns this week, pushing...

US payrolls missed sharply at 57K this week, lifting rate cut expectations and supporting a broadly...

The RBA held the cash rate steady at 4.35% this week, supporting Australian equities while the Bank...