A global markets summary, for

Australian investors

The Australian budget CGT and negative gearing overhaul dominated this week, as Treasurer Chalmers delivered the most significant tax restructure in decades alongside persistent wage growth and hotter US inflation data.

Five key developments:

1. Grim Jim releases a shocker budget

Treasurer Jim Chalmers delivered one of the most aggressive tax overhauls in decades, with the market particularly focused on changes to capital gains tax, negative gearing and discretionary trusts. The Budget proposed replacing the 50% CGT discount from 1 July 2027 with an inflation indexation model alongside a new 30% minimum tax on capital gains, materially changing the after-tax economics of property, shares, ETFs and private business exits. Negative gearing on existing residential properties would also be effectively removed for future purchases, while discretionary trusts face a new 30% minimum tax from 1 July 2028.

2. Chinese CPI rises to 1.2% y/y

Chinese inflation rose to 1.2% year-on-year, signalling a modest improvement in domestic demand after a prolonged period of weak price growth. While the result suggests some stabilisation, inflation remains low by global standards, keeping pressure on policymakers to support consumption and property activity, with the outlook still dependent on sustained stimulus transmission.

3. US Core CPI m/m rises to 0.4% m/m

US Core CPI rose 0.4% month-on-month, a stronger inflation print that challenged expectations for near-term rate relief. The result reinforced concerns that services inflation and underlying price pressures remain persistent, pushing bond yields higher and weighing on equities, with the outlook favouring a more cautious Federal Reserve stance.

4. US Core Retail sales rise 0.7% m/m

US Core Retail Sales rose 0.7% month-on-month, pointing to resilient consumer demand despite higher borrowing costs and softer sentiment. The strength in spending supports near-term growth but also complicates the inflation outlook, as firm demand gives businesses more pricing power, with the outlook suggesting fewer reasons for the Fed to ease quickly.

5. Australian Wage Price Index q/q steady at 0.8% m/m

Australia’s Wage Price Index held steady at 0.8% quarter-on-quarter, showing wage growth remains firm but not accelerating. The result is unlikely to alarm the RBA on its own, but combined with fiscal stimulus and sticky services inflation, it keeps domestic inflation risks alive, with the outlook pointing to a cautious policy bias.

Australian Focus

The Federal Budget dominated the domestic week, with Treasurer Chalmers overhauling CGT, negative gearing, and trust taxation in a move that materially reshapes the after-tax economics of property, shares, and private business exits for Australian investors.

For Australian investors, the combined pressure of fiscal tightening, sticky wages, and hotter US inflation keeps the RBA on hold while the budget changes demand an immediate review of portfolio and structure decisions — particularly around CGT timing, trust distributions, and property exposure ahead of the 2027 implementation date.

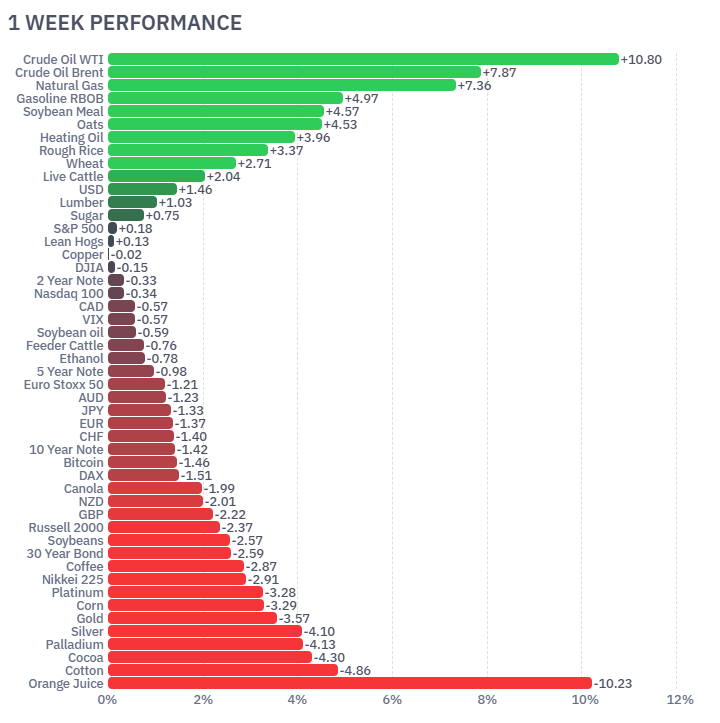

Futures Market Performance

Energy led futures markets higher with crude oil surging over 10%, while metals and equity indices softened as hotter US inflation pushed bond yields higher.

Futures markets were mixed, with energy strongly outperforming as Crude Oil WTI (+10.80%), Brent (+7.87%) and Natural Gas (+7.36%) rallied on tighter supply concerns and firmer demand expectations. Grains were also stronger, led by Wheat (+2.71%) and Oats (+4.53%), while softs were weaker, with Orange Juice (-10.23%), Cotton (-4.86%) and Cocoa (-4.30%) falling sharply. Equity futures softened, including Nasdaq 100 (-0.34%), Russell 2000 (-2.37%) and Nikkei 225 (-2.91%), as hotter inflation and stronger retail sales pushed yields higher. Metals were broadly weaker, with Gold (-3.57%), Silver (-4.10%) and Copper (-3.29%) under pressure.

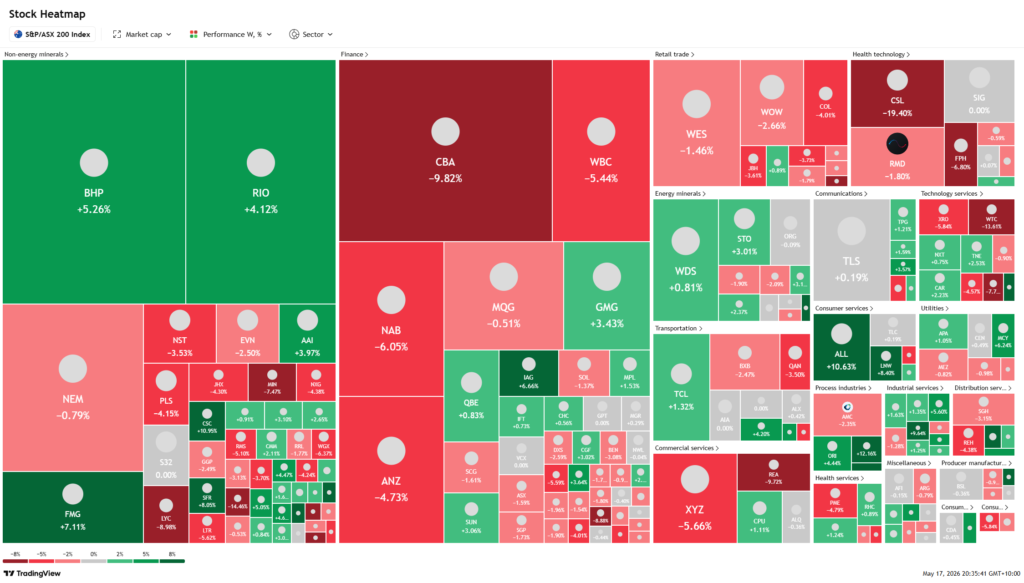

ASX Weekly Heatmap

The ASX 200 split sharply, with miners rallying on commodity strength while banks and growth stocks fell heavily as budget concerns and rising yields weighed on rate-sensitive sectors.

Large miners rallied, with BHP (+5.26%), RIO (+4.12%) and FMG (+7.11%) supported by stronger commodity sentiment and Chinese inflation stabilisation. Banks were heavy, with CBA (-9.82%), NAB (-6.05%), ANZ (-4.73%) and WBC (-5.44%) dragging the index as higher yields and budget concerns weighed on rate-sensitive financials. Health care also fell sharply, led by CSL (-19.40%). Standout winners included ALL (+10.63%), IAG (+6.66%) and GMG (+3.43%), while REA (-9.72%), XRO (-5.84%) and WTC (-13.61%) showed broader growth-stock pressure.

If any of this week’s developments raise questions about your portfolio, please get in touch.

Related Insights

Iran's renewed blockade of the Strait of Hormuz reignited energy supply concerns this week, pushing...

US payrolls missed sharply at 57K this week, lifting rate cut expectations and supporting a broadly...

The RBA held the cash rate steady at 4.35% this week, supporting Australian equities while the Bank...