A global markets summary, for

Australian investors

Australian GDP growth disappointed sharply this week at 0.3% against expectations of 0.9%, while US employment surging to 172K reinforced a higher-for-longer rates outlook and triggered a broad selloff across growth and risk assets.

Five key developments:

1. US tech fall most since April 2025

US technology stocks experienced their sharpest one-day decline since April 2025, as stronger-than-expected employment data and rising bond yields triggered a repricing of rate expectations. The selloff highlighted ongoing valuation sensitivity across growth sectors, reinforcing concerns that interest rates may remain restrictive for longer as the outlook for policy easing becomes less certain.

2. US Manufacturing PMI rises to 54 vs 52.7 previous

US manufacturing activity strengthened further, signalling improving industrial momentum and resilient business conditions despite restrictive monetary policy. The stronger reading supports confidence that the broader economy remains stable, reducing immediate recession concerns while reinforcing expectations that economic activity continues to expand as the outlook remains constructive.

3. Australian GDP grows slowly at 0.3% vs 0.9% expected

Australian economic growth disappointed materially, highlighting the impact of higher interest rates and softer household demand on domestic activity. Slowing growth supports the view that inflation pressures should gradually moderate over time, reducing the likelihood of further aggressive RBA tightening as the outlook for the domestic economy weakens.

4. Canadian Unemployment Rate drops to 6.6%

Canada’s unemployment rate unexpectedly improved, signalling labour market conditions remain more resilient than anticipated despite slowing global growth conditions. Stronger employment conditions support household consumption and broader economic stability, reducing immediate recession concerns as the outlook for the Canadian economy remains relatively balanced.

5. US Non-Farm Employment Change rises to 172K vs 85K expected

US payrolls significantly exceeded expectations, reinforcing confidence in the resilience of the labour market and underlying economic momentum. Strong employment growth continues supporting consumption and activity levels, although the result may reduce expectations for near-term Federal Reserve easing as policymakers remain focused on inflation risks.

Australian Focus

Australian GDP growing at just 0.3% against expectations of 0.9% was the standout domestic data point this week, confirming that higher interest rates are weighing materially on household demand and broader economic activity. The weak print reduces the case for further RBA tightening but does little to resolve the inflation challenge in the near term.

For Australian investors, the combination of soft Australian GDP and US employment running well above expectations creates a difficult cross-current. Rising US bond yields driven by the strong payrolls result pressured resources, banks, and growth stocks simultaneously, as visible in the ASX heatmap. Defensives and high-quality earnings names held up better, and that rotation is likely to continue while domestic growth stays soft and global rate expectations stay elevated.

Futures Market Performance

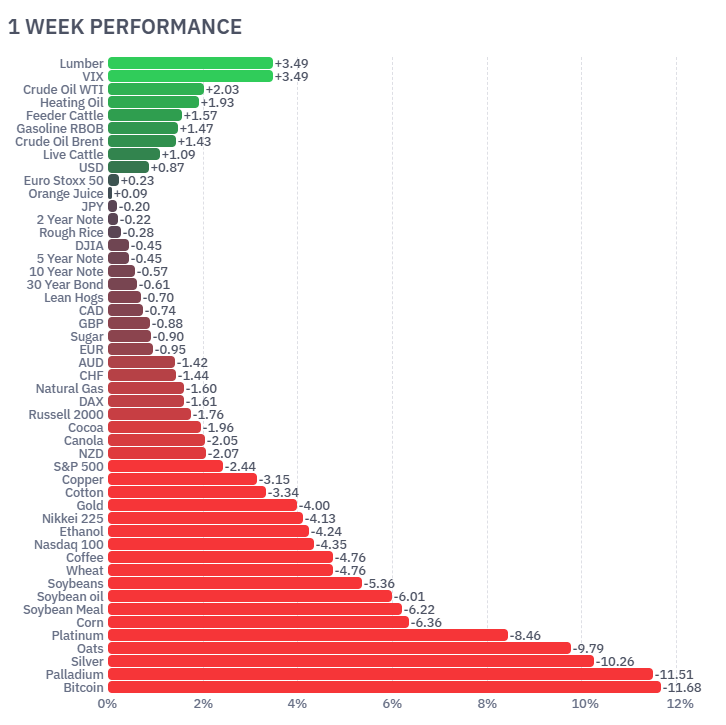

Markets adopted a more defensive tone over the week as stronger US economic data reduced expectations for near-term rate cuts and pressured growth assets. Volatility increased sharply with the VIX (+3.49%), while energy markets rallied, led by Crude Oil WTI (+2.03%), Heating Oil (+1.93%) and Brent (+1.43%). Conversely, risk-sensitive assets weakened materially, with Bitcoin (-11.68%), Palladium (-11.51%) and Silver (-10.26%) suffering heavy losses. Equity futures were broadly weaker, with the Nasdaq (-4.35%), Nikkei 225 (-4.13%) and S&P 500 (-2.44%) all declining as bond yields moved higher.

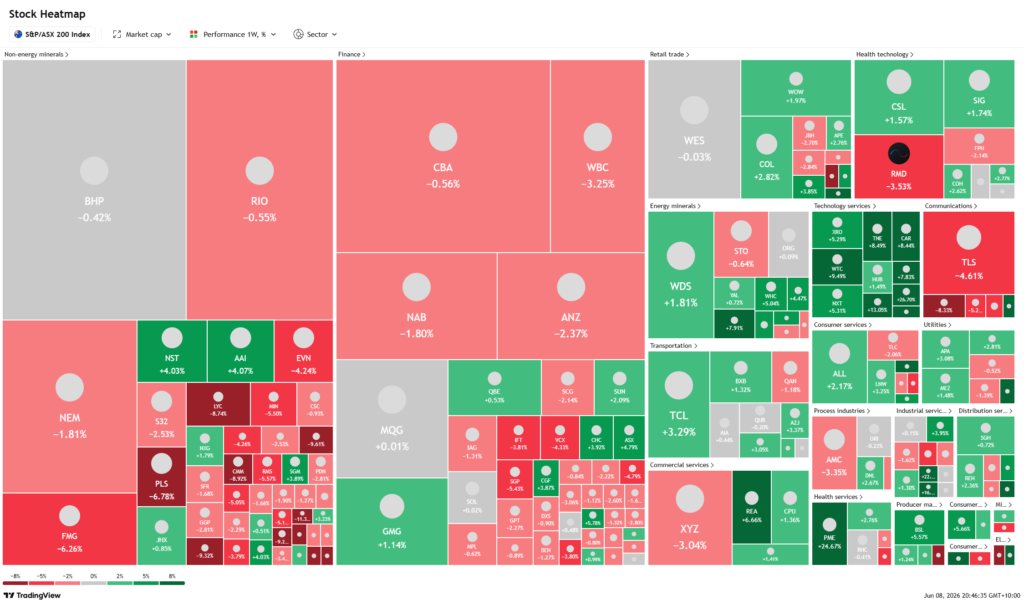

ASX Weekly Heatmap

The ASX weakened broadly over the week, with the heaviest pressure concentrated across resources and financials following the stronger-than-expected US payrolls data and subsequent rise in global bond yields. Iron ore and lithium-related names were particularly weak, with FMG (-6.26%), PLS (-6.78%), MIN (-5.50%) and LYC (-8.74%) sold aggressively as commodity and growth expectations softened. The banks also struggled under the weight of weaker domestic GDP data, with WBC (-3.25%), ANZ (-2.37%) and NAB (-1.80%) lower as investors reassessed earnings expectations against a slowing Australian economy. In contrast, select defensive and growth names outperformed, including XRO (+5.29%), WTC (+9.49%) and TCL (+3.29%), highlighting continued rotation into higher-quality earnings and structural growth exposures despite broader market weakness.

If any of this week’s developments raise questions about your portfolio, please get in touch.

Related Insights

The US Iran peace deal dominated global markets this week, rapidly unwinding geopolitical risk premi...

Australian CPI inflation rose 0.4% m/m this week, missing expectations and reinforcing the higher-fo...

The Strait of Hormuz reopening eased geopolitical risk premiums this week as Australian unemployment...