A global markets summary, for

Australian investors

The Strait of Hormuz reopening eased geopolitical risk premiums this week as Australian unemployment rises, shifting the domestic outlook toward softer growth and reduced RBA tightening pressure.

Five key developments:

1. Iran and US strike deal to open Strait of Hormuz

Iran and the US reached a temporary agreement to reopen the Strait of Hormuz following weeks of military escalation and threats to shipping routes. The arrangement includes unrestricted tanker passage and a pause in further military action while negotiations continue. If maintained, the agreement could reduce geopolitical risk premiums, ease inflation concerns and support broader market sentiment as the outlook stabilises.

2. British Claimant Count Change rises to 26.5K

UK claimant counts increased sharply, highlighting ongoing softness in labour market conditions and weaker employment momentum. Rising unemployment pressures are likely to weigh on household spending and broader growth, increasing expectations that policymakers may eventually need to support activity as the outlook for the UK economy becomes more subdued.

3. Australian unemployment rate rises to 4.5%

Australia’s unemployment rate moved higher, signalling labour market conditions are beginning to soften after an extended period of resilience. Rising unemployment reduces wage pressure and supports the disinflation process, potentially easing pressure on the RBA to tighten further as the outlook shifts toward slower domestic growth.

4. US Pending Home Sales rise to 1.4% m/m

US housing activity surprised to the upside, suggesting demand remains resilient despite elevated mortgage rates. Stronger housing turnover points to underlying consumer stability and improving confidence, supporting broader economic activity while reducing immediate recession concerns as the outlook remains relatively constructive.

5. Australian Unemployment Change -18.6K

Australia shed jobs during the month, reinforcing signs of cooling labour demand and slowing economic momentum. Softer employment conditions are likely to moderate consumption and wage growth over time, supporting expectations that monetary policy may become less restrictive if weakness persists as the outlook turns more balanced.

Australian Focus

The US-Iran deal to reopen the Strait of Hormuz was the week’s pivotal development, unwinding energy risk premiums and lifting global risk sentiment sharply after weeks of supply disruption fears keeping markets on edge.

For Australian investors, the geopolitical relief rally favours financials and consumer-facing names — as reflected in the ASX rebound — but softening domestic labour data tells a more cautious story underneath. Rising unemployment and job losses reduce RBA tightening pressure but also signal slowing domestic momentum that warrants watching.

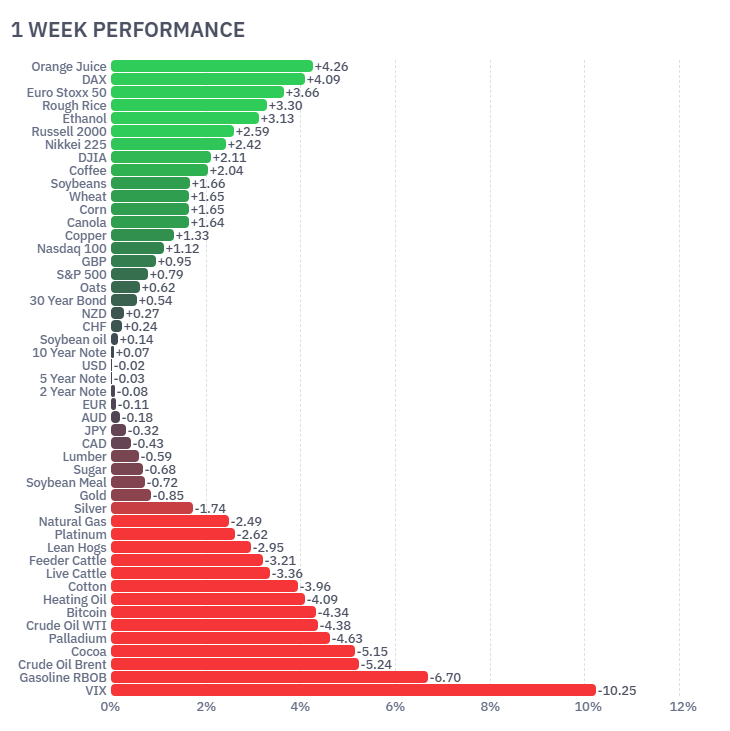

Futures Market Performance

Risk sentiment improved sharply following the Hormuz deal, lifting equities and collapsing volatility while oil prices fell as supply fears unwound.

Risk sentiment improved markedly following the easing in Middle East tensions, driving a broad rebound across global equity markets and cyclical assets. European equities led gains with the DAX (+4.09%) and Euro Stoxx 50 (+3.66%) rallying strongly, while the Nikkei (+2.42%) and Russell 2000 (+2.59%) also advanced. Commodity markets were mixed, with Orange Juice (+4.26%) and Coffee (+2.04%) stronger, while volatility collapsed (VIX -10.25%) alongside sharp declines in oil markets, with Brent (-5.24%) and WTI (-4.38%) falling as supply fears eased.

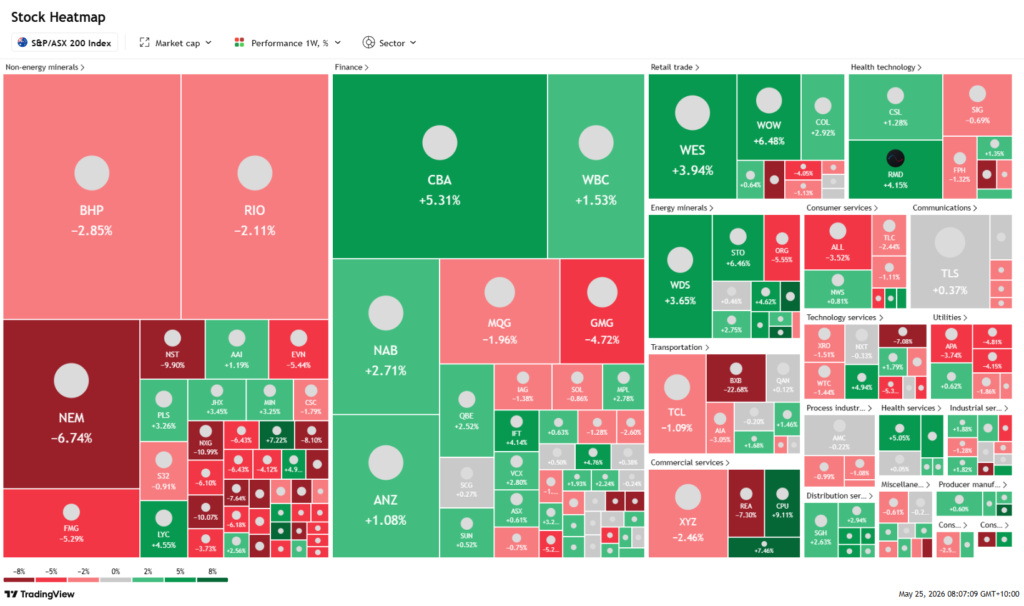

ASX Weekly Heatmap

The ASX rebounded strongly, led by banks and retailers as geopolitical risk premiums eased, while resource names lagged on softer commodity prices following the Hormuz reopening.

Banks rallied sharply with NAB (+2.71%), CBA (+5.31%) and WBC (+1.53%) higher, while retailers WES (+3.94%) and WOW (+6.48%) outperformed on improving sentiment. Resource names lagged, with BHP (-2.85%), RIO (-2.11%) and NEM (-6.74%) weaker as commodity prices softened following the reopening of the Strait of Hormuz and easing energy concerns.

If any of this week’s developments raise questions about your portfolio, please get in touch.

Related Insights

The US Iran peace deal dominated global markets this week, rapidly unwinding geopolitical risk premi...

Australian GDP growth disappointed sharply this week at 0.3% against expectations of 0.9%, while US...

Australian CPI inflation rose 0.4% m/m this week, missing expectations and reinforcing the higher-fo...