A global markets summary, for

Australian investors

Australian CPI inflation rose 0.4% m/m this week, missing expectations and reinforcing the higher-for-longer rates outlook as domestic price pressures remain persistent despite restrictive RBA policy settings.

Five key developments:

1. Australian CPI rises by 0.4% m/m, missing expectations

Australian inflation rose during the month, reinforcing the view that domestic price pressures remain persistent despite restrictive monetary policy settings. Sticky services and housing-related inflation continue to challenge policymakers, reducing the likelihood of near-term easing and supporting a higher-for-longer rates outlook as inflation progress remains gradual.

2. RBNZ holds cash rate steady at 2.25%

The RBNZ kept policy settings unchanged, signalling confidence that inflation pressures are moderating while economic growth remains soft. Holding rates steady allows policymakers time to assess the impact of prior tightening, supporting a neutral policy stance as the outlook remains balanced between inflation control and slowing activity.

3. US Core PCE Price Index steady at 0.2% m/m

The Fed’s preferred inflation measure remained steady, reinforcing evidence that underlying inflation is continuing to moderate gradually. Stable core pricing supports expectations that policy settings are sufficiently restrictive, allowing the Federal Reserve to remain patient as the outlook for inflation trends continues to improve.

4. US New Home Sales steady at 622k vs 661k expected

US housing activity disappointed expectations, highlighting ongoing pressure from elevated mortgage rates and tighter financial conditions. Softer housing demand points to moderating consumer momentum and weaker construction activity, supporting a more cautious economic outlook as higher borrowing costs continue weighing on interest-sensitive sectors.

5. German Prelim CPI contracts by -0.2% m/m

German inflation unexpectedly contracted, reinforcing broader disinflationary trends across Europe and increasing expectations for accommodative policy settings. Weak price momentum reflects subdued economic activity and softer demand conditions, supporting the case for a more supportive monetary environment as the outlook for European growth remains fragile.

Australian Focus

Australian CPI rising 0.4% m/m and missing expectations keeps the RBA’s higher-for-longer bias intact, even as energy prices continue unwinding post-Hormuz and European disinflation points to a global easing trend Australia remains behind.

For Australian investors, sticky domestic services and housing inflation delay any rate relief. The sector rotation visible in the ASX, with resources and retailers firm while banks and healthcare lag, reflects a market adjusting to a prolonged hold rather than an imminent cut.

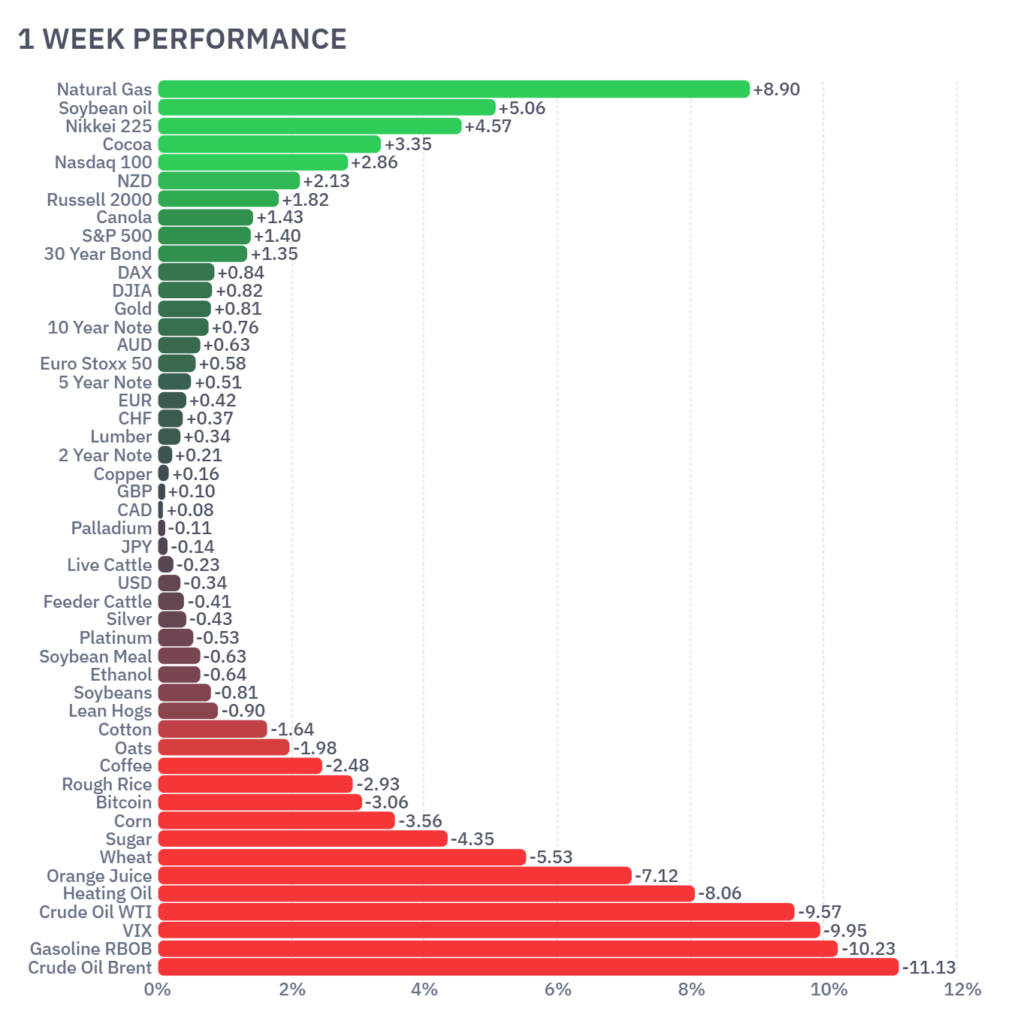

Futures Market Performance

Equity markets advanced on easing inflation concerns while energy sold off sharply as Hormuz risk premiums continued unwinding, with Brent and WTI both falling over 9%.

Risk sentiment improved across equity markets despite ongoing weakness in energy markets and volatility. The Nikkei 225 (+4.57%), Nasdaq (+2.86%) and Russell 2000 (+1.82%) advanced on improving growth sentiment and easing inflation concerns. Commodity markets were mixed, with Natural Gas (+8.90%) and Soybean Oil (+5.06%) outperforming. Energy products sold off sharply, including Brent (-11.13%), RBOB Gasoline (-10.23%) and WTI (-9.57%) as geopolitical risk premiums continued unwinding. Volatility also eased materially, with the VIX falling (-9.95%).

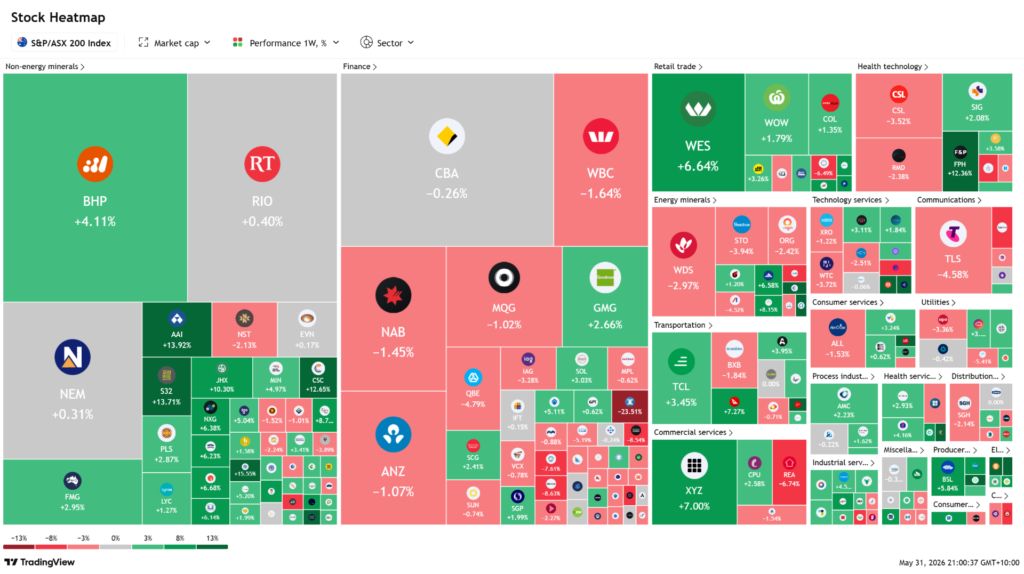

ASX Weekly Heatmap

The ASX was mixed with resources and retailers outperforming while financials and healthcare lagged, reflecting ongoing sector rotation beneath a stable index backdrop

BHP (+4.11%) outperformed alongside AAI (+13.92%) and S32 (+13.71%), supporting the materials sector, while retailers WES (+6.64%) and WOW (+1.79%) were firm. Financials lagged, with NAB (-1.45%), ANZ (-1.07%) and WBC (-1.64%) weaker, while healthcare remained under pressure through CSL (-3.52%) and TLS (-4.58%), highlighting ongoing sector rotation beneath a relatively stable index backdrop.

If any of this week’s developments raise questions about your portfolio, please get in touch.

Related Insights

The US Iran peace deal dominated global markets this week, rapidly unwinding geopolitical risk premi...

Australian GDP growth disappointed sharply this week at 0.3% against expectations of 0.9%, while US...

The Strait of Hormuz reopening eased geopolitical risk premiums this week as Australian unemployment...