A global markets summary, for

Australian investors

This week’s RBA rate hike Australia’s inflation outlook front and centre, as the cash rate rises to 4.35% and markets weigh whether the tightening cycle has peaked.

Five key developments:

1. RBA increases the cash rate to 4.35%

The RBA raised the cash rate by 25bps to 4.35%, citing persistent inflation pressures and resilient domestic demand. Financial conditions continue to tighten as mortgage costs rise further, while markets remain divided on whether this marks the peak of the cycle. The outlook remains cautious, with future policy decisions likely to remain highly dependent on inflation and labour market data.

2. NZ unemployment rate drops to 5.3%

New Zealand unemployment unexpectedly declined to 5.3%, suggesting labour market conditions remain firmer than anticipated despite slowing economic growth. The result supported the NZD and reduced expectations for aggressive near-term rate cuts from the RBNZ. The outlook points toward a gradual easing cycle, with policymakers likely to remain cautious while inflation pressures persist across parts of the economy.

3. US Average Hourly Earnings drop to 0.2% m/m

US Average Hourly Earnings slowed to 0.2% month-on-month, reinforcing expectations that wage-driven inflation pressures may be easing. Equity markets responded positively as softer wage growth supports the prospect of a less aggressive Federal Reserve policy path. The outlook remains supportive for risk assets if inflation continues moderating without a meaningful deterioration in broader economic activity.

4. Iran and US continue to provide mixed messages

Mixed commentary from both Iran and the United States continued to create uncertainty across commodity and risk markets throughout the week. Oil prices experienced heightened volatility as traders reacted to conflicting geopolitical headlines and shifting expectations surrounding regional stability. The outlook remains highly headline-sensitive, with energy and volatility markets likely to remain reactive to any escalation in tensions.

5. US equities continue to storm higher, thanks to AI stocks

US equities continued rallying strongly, led once again by AI-related technology companies and semiconductor stocks. Investor optimism surrounding artificial intelligence spending and earnings growth continued driving momentum in major indices, particularly the Nasdaq 100. The outlook remains constructive for equities in the near term, although elevated valuations within AI-linked sectors continue to increase concentration and sustainability concerns.

Australian Focus

The RBA’s hike to 4.35% was the week’s defining domestic move, with the board citing persistent inflation and resilient demand, leaving markets divided on whether the cycle has peaked or has further to run.

For Australian investors, tightening mortgage conditions weigh on consumer discretionary and property-linked names, while softer US wage growth and the AI-driven equity rally offer a constructive offshore backdrop. Energy remains volatile on mixed Iran headlines, and rate-sensitive domestic sectors stay under pressure until the RBA signals a clear pause.

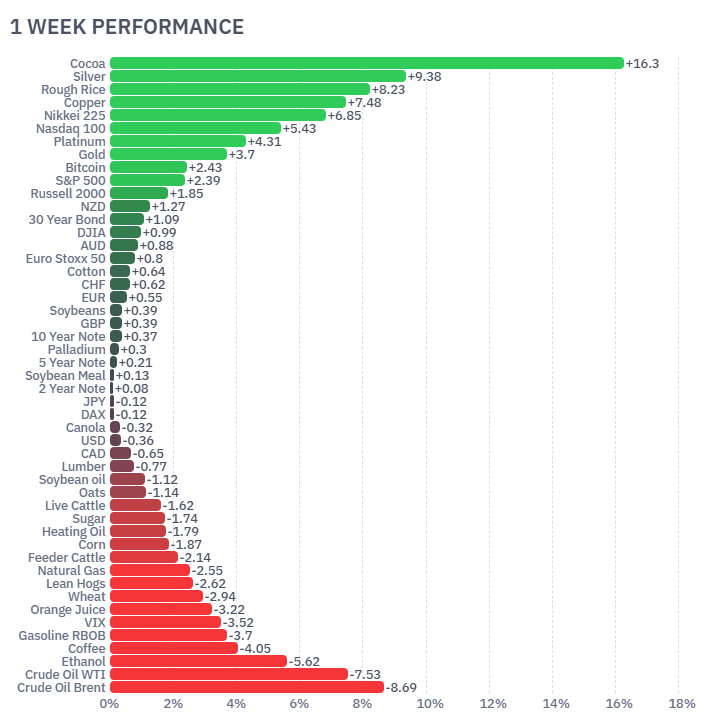

Futures Market Performance

Futures markets were mixed over the week, with strong gains across metals and equity indices offset by a sharp selloff in energy markets. Cocoa (+16.3%), Silver (+9.38%), Copper (+7.48%) and the Nasdaq 100 (+5.43%) rallied as investors continued favouring AI-linked growth themes and industrial metals exposure. Equity sentiment also improved following softer US wage growth data. In contrast, Brent Crude (-8.69%) and WTI Crude (-7.53%) fell sharply as geopolitical risk premium faded despite ongoing Iran-US tensions. Coffee (-4.05%), Natural Gas (-2.55%) and Wheat (-2.94%) also weakened amid improving supply expectations.

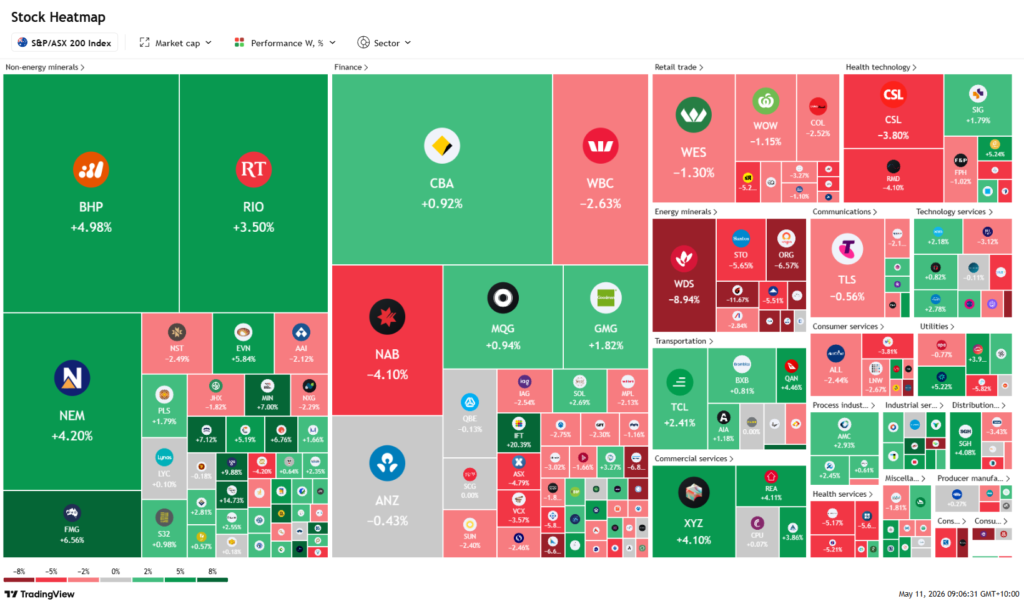

ASX Weekly Heatmap

The ASX 200 delivered a mixed performance, with miners providing the strongest support to the index. BHP (+4.98%), Rio Tinto (+3.50%), Newmont (+4.20%) and Fortescue (+6.56%) rallied on stronger commodity sentiment and renewed optimism surrounding Chinese demand. Financials were divided, with Commonwealth Bank (+0.92%) and Macquarie (+0.94%) higher, while NAB (-4.10%) and Westpac (-2.63%) weakened following the RBA rate increase. Energy stocks underperformed sharply as oil prices fell, with Woodside (-8.94%), Santos (-5.65%) and Origin (-6.57%) among the weakest large-cap performers.

If any of this week’s developments raise questions about your portfolio, please get in touch.

Related Insights

Iran's renewed blockade of the Strait of Hormuz reignited energy supply concerns this week, pushing...

US payrolls missed sharply at 57K this week, lifting rate cut expectations and supporting a broadly...

The RBA held the cash rate steady at 4.35% this week, supporting Australian equities while the Bank...