A global markets summary, for

Australian investors

The Hormuz energy shock Australia is facing this week stems from Iranian escalation in the Strait, threatening global oil supply and lifting stagflation risk across developed economies.

Five key developments:

1. Iran fires bullets in the Strait

Escalation in the Strait of Hormuz has materially lifted geopolitical risk, with energy markets reacting sharply to potential supply disruptions. Roughly 20% of global oil flows transit this corridor, and any interference drives immediate pricing pressure and inflation expectations higher. The IMF has warned of a global energy shock impacting all economies, reinforcing stagflation risks and tightening financial conditions into the outlook.

2. US Core PPI m/m contracts to 0.1%

Producer prices cooling to 0.1% m/m suggests some short-term easing in upstream inflation pressures. However, this remains inconsistent with broader survey data showing rising input costs and energy-driven inflation risks building beneath the surface. Markets are increasingly treating this as a lagging data point, with forward-looking inflation expectations still skewed higher given supply shocks, pointing to a fragile disinflation trend.

3. Australian unemployment in line with expectations at 17.9K

Australian employment growth landing broadly in line reflects a still-resilient labour market, consistent with the RBA’s expectation of gradual cooling rather than sharp deterioration. Stability in hiring supports consumption and domestic demand, but with global uncertainty rising and commodity volatility increasing, forward indicators suggest labour momentum may soften. The outlook remains balanced but increasingly exposed to external shocks.

4. British GDP m/m 0.5% vs 0.1% previous

UK GDP surprised materially to the upside at 0.5%, driven by broad-based gains across services, manufacturing, and construction. However, this data is backward-looking and reflects pre-conflict conditions. With energy prices surging post-Iran escalation, economists expect this momentum to fade, with the Bank of England facing a tightening vs growth trade-off, leaving the outlook skewed toward slower growth and higher inflation.

5. US Unemployment claims 207K vs 213K

Jobless claims falling to 207K reinforces the narrative of a still-tight US labour market, with layoffs remaining subdued despite geopolitical uncertainty. However, underlying trends point to a “low hire, low fire” environment, where labour demand is steady but not accelerating. This keeps the Fed in a holding pattern, with resilience supporting growth but limiting urgency for rate cuts in the near-term outlook.

Australian Focus:

The Hormuz energy shock Australia experienced this week sharpened energy risk materially, with the IMF flagging a potential global supply crisis that keeps stagflation firmly on the table. US labour markets held tight while cooling PPI offered limited comfort against the broader supply-side inflation building beneath the surface.

For Australian investors, steady domestic employment is supportive but increasingly secondary to the external risk picture. The Hormuz energy shock Australia faces reinforces the case for energy exposure and a defensive portfolio tilt, with the RBA having no room to ease while inflation risks skew higher.

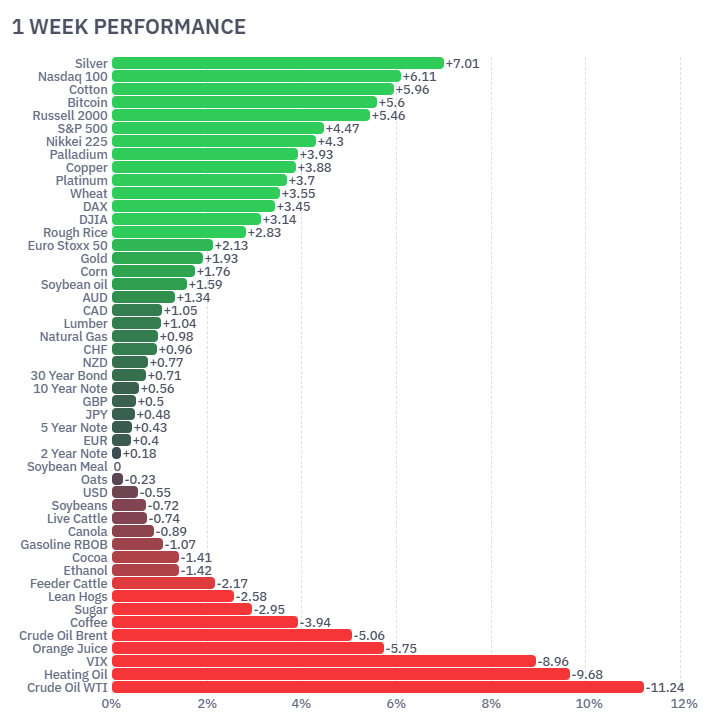

Futures Market Performance

Futures markets reflected a clear stagflationary tilt, with hard assets outperforming and energy sharply lower late-week on positioning shifts. Silver (+7.01%), Nasdaq (+6.11%), and Bitcoin (+5.6%) led risk-on momentum, while industrial metals and grains posted solid gains (Copper +3.88%, Wheat +3.55%). In contrast, energy collapsed with Crude Oil WTI (-11.24%), Heating Oil (-9.68%) and VIX (-8.96%), suggesting volatility compression and potential de-escalation pricing despite ongoing geopolitical risks. Soft commodities lagged (Coffee -3.94%, Sugar -2.95%), highlighting divergence across real asset classes driven by supply dynamics and macro positioning.

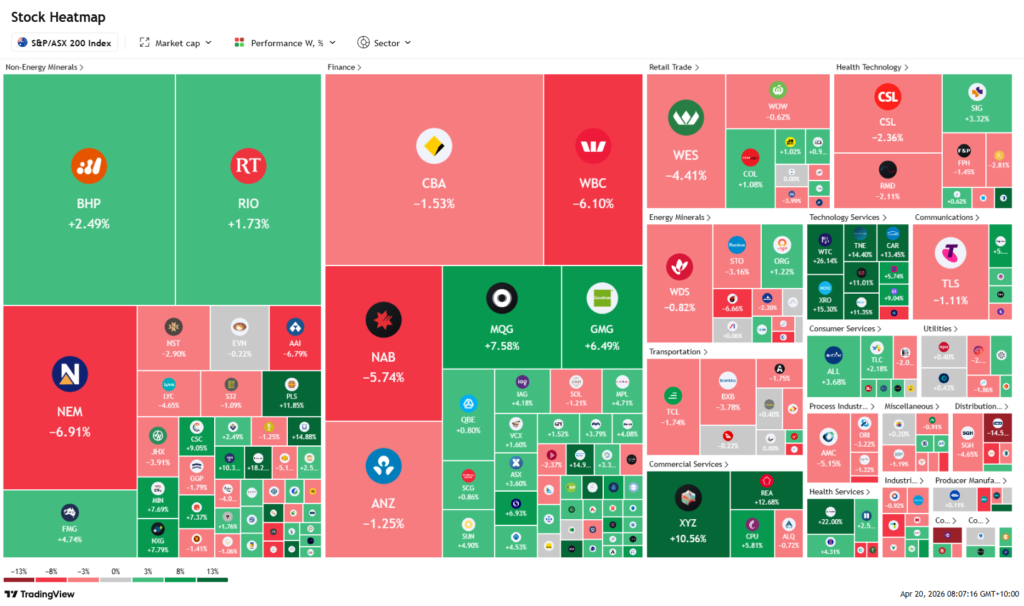

ASX Weekly Heatmap

The ASX showed a bifurcated market, with resources providing support while financials dragged. Large-cap miners outperformed, with BHP (+2.49%) and Rio (+1.73%) benefiting from stronger commodity prices. In contrast, banks were weak across the board (CBA -1.53%, NAB –5.74%, WBC -6.10%) reflecting margin pressure and risk-off positioning. Growth pockets emerged in financials and tech (MQG +7.58%, GMG +6.49%), while energy and healthcare were mixed, with CSL (-2.36%) and WDS (-0.82%) lagging. The overall tone suggests rotation rather than broad risk appetite, with capital selectively targeting momentum and real asset exposure.

If any of this week’s developments raise questions about your portfolio, please get in touch.

Related Insights

Iran's renewed blockade of the Strait of Hormuz reignited energy supply concerns this week, pushing...

US payrolls missed sharply at 57K this week, lifting rate cut expectations and supporting a broadly...

The RBA held the cash rate steady at 4.35% this week, supporting Australian equities while the Bank...