US Core CPI steady at 0.2% m/m

Core inflation held steady, reinforcing the view that underlying price pressures are easing but not disappearing. A stable print keeps the Fed in “wait-and-watch” mode, as policymakers balance inflation progress against still-firm activity. Markets are likely to stay sensitive to any re-acceleration in services inflation as the outlook remains cautiously constructive.

US Core retail sales rise to 0.5% m/m

Core retail sales strengthened, signaling the US consumer remains resilient despite higher rates. Firm spending momentum supports growth but complicates the inflation path by keeping demand elevated. With consumption holding up, the Fed has less urgency to move aggressively, and policy expectations may stay anchored to gradualism as the outlook stays data-dependent.

Trump imposes 10% tariffs on EU nations who don’t support his action on Greenland

The tariff announcement lifts geopolitical and trade uncertainty, increasing the risk premium across global markets. Even if near-term economic effects are limited, the threat of retaliation and supply chain disruption can dampen business confidence. This kind of policy volatility tends to support defensives and gold while keeping risk sentiment fragile as the outlook turns more uncertain.

US unemployment claims drop to 198K

Claims fell to very low levels, underscoring ongoing tightness in the labour market. Continued employment resilience supports household income and spending, but also reduces the case for rapid easing if wage pressure persists. With labour conditions still firm, policy may remain restrictive for longer, leaving markets focused on inflation follow-through as the outlook stays balanced.

British GDP rises to 0.3% m/m

UK growth improved modestly, easing recession concerns and suggesting activity is stabilising. A firmer growth backdrop gives the Bank of England flexibility to stay cautious on easing until inflation is clearly contained. If growth persists while inflation cools, policy can normalise slowly, supporting risk appetite at the margin as the outlook gently improves.

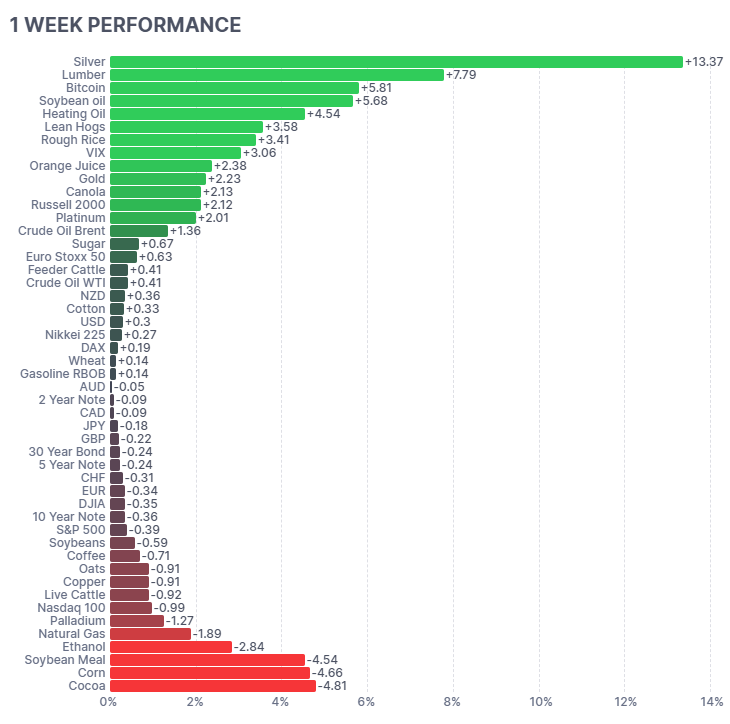

Below shows the monthly performance of a range of futures markets we track.

Commodity markets diverged sharply over the week, with softs and precious metals leading gains while energy and grains sold off. Orange Juice (+11.98%), Cocoa (+10.55%) and Platinum (+6.25%) surged on supply constraints and positioning dynamics, while Gold (+2.05%) remained supported by rate-cut confirmation. Energy markets were heavily pressured, with Natural Gas (-22.46%), Heating Oil (-6.70%) and WTI (-4.24%) sliding on oversupply and weaker demand expectations. Equity risk was mixed, with the S&P 500 (-1.51%) and Nasdaq 100 (-3.02%) under pressure as volatility rose (VIX +3.26%) amid sector rotation and rate repricing.

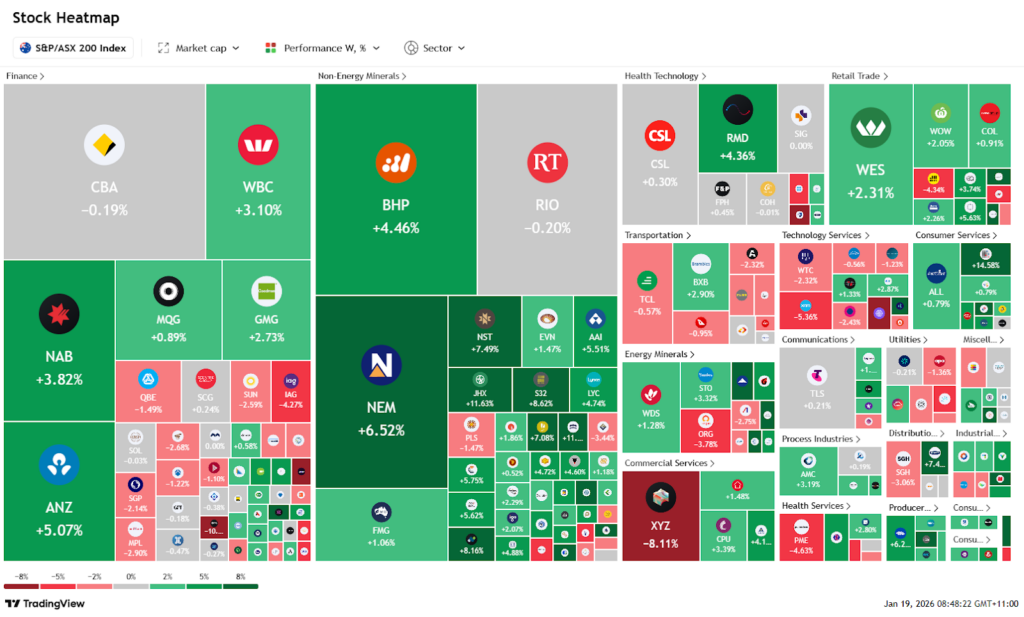

Here is the week’s heatmap for the largest companies in the ASX.

Australian equities were broadly constructive, driven by banks and large-cap resources. Financials outperformed, led by NAB (+4.28%), WBC (+3.55%) and CBA (+2.84%) as stable rates supported margins. Resource majors were firm, with BHP (+2.33%), RIO (+3.76%) and FMG (+5.51%) benefiting from improved China inflation data. Stock-specific strength was evident in NEM (+8.68%) and SIG (+5.04%), while technology and consumer names lagged, with WTC (-4.03%), XRO (-6.48%) and WES (-0.84%) reflecting earnings sensitivity and valuation pressure.

Related Insights

Canadian CPI drops to 2.8% y/y Canadian inflation continued to cool, reinforcing the broader disinfl...

Australia RBA Cash Rate held at 3.60% The RBA kept policy steady, reinforcing its patient stance as...