Canadian CPI drops to 2.8% y/y

Canadian inflation continued to cool, reinforcing the broader disinflation trend across developed markets. Softer price pressures ease concerns around sticky services inflation and give the Bank of Canada greater flexibility to shift policy toward support rather than restraint, which should gradually improve financial conditions and underpin risk appetite as growth stabilises.

German Flash Manufacturing PMI declines to 47.7 vs 48.2 previous

German manufacturing slipped further into contraction, highlighting persistent weakness in the Eurozone’s industrial core. Subdued external demand, cautious capital spending, and ongoing cost pressures continue to weigh on output, keeping recession risks elevated and reinforcing expectations that monetary policy will remain accommodative as growth headwinds persist.

US average hourly earnings m/m decline to 0.1%

US wage growth slowed meaningfully, reducing the risk of second-round inflation effects and easing pressure on the Federal Reserve. Cooling earnings momentum supports the soft-landing narrative, suggesting labour demand is normalising rather than overheating, which allows policymakers greater confidence that inflation can continue trending lower over time.

US non-farm employment change jumps to 64K vs 51K expected

US employment surprised modestly to the upside, signalling continued labour market resilience despite broader slowing momentum. Job creation remains positive but contained, pointing to a gradual rebalancing rather than renewed strength, which supports steady consumption while remaining consistent with a lower-inflation environment going forward.

US CPI drops to 2.7% y/y

US inflation declined further, reinforcing confidence that the peak in price pressures is well behind us. Broad-based moderation across goods and services strengthens expectations for an eventual easing cycle, supporting equity valuations and duration-sensitive assets as markets increasingly price a more dovish policy path ahead.

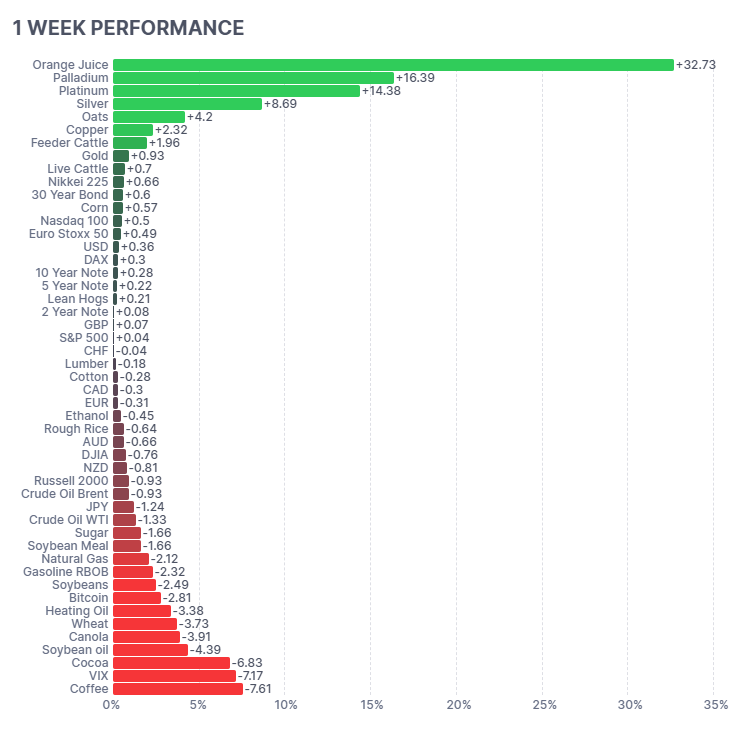

Below shows the monthly performance of a range of futures markets we track.

Futures markets showed sharp dispersion over the week. Agricultural softs led gains with Orange Juice (+32.73%) surging on supply disruptions, while Palladium (+16.39%), Platinum (+14.38%), and Silver (+8.69%) benefited from easing real rates. Energy and grains were weaker, with Coffee (-7.61%), Cocoa (-6.83%), Soybean Oil (-4.39%), and Wheat (-3.73%) pressured by improving supply outlooks and softer demand. Volatility eased as VIX fell (-7.17%), while Bitcoin (-2.81%) consolidated amid a calmer risk backdrop.

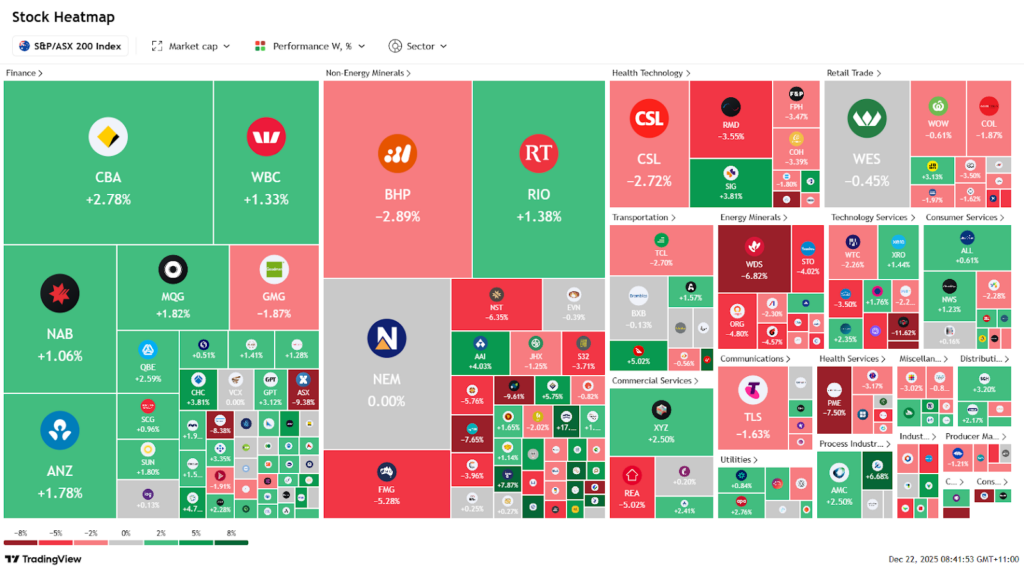

Here is the week’s heatmap for the largest companies in the ASX.

Australian equities showed clear sector dispersion. Financials led, with CBA (+2.78%), MQG (+1.82%), ANZ (+1.78%), WBC (+1.33%) and NAB (+1.06%) supported by easing global inflation and softer US wage growth, reducing rate pressure while labour markets remained resilient. Materials were mixed: RIO (+1.38%) held up, but BHP (-2.89%) and FMG (-5.28%) lagged as weak German manufacturing PMI (47.7) weighed on the global industrial outlook and bulk commodity demand. Energy was the main drag, with WDS (-6.82%), STO (-4.02%) and ORG (-4.80%) tracking softer oil prices amid cooling growth expectations. Healthcare underperformed as investors rotated away from defensives into cyclicals.

Related Insights

"US strikes on Iranian nuclear facilities drove oil prices sharply higher this week, while flat US c...

Iran's renewed blockade of the Strait of Hormuz reignited energy supply concerns this week, pushing...

US payrolls missed sharply at 57K this week, lifting rate cut expectations and supporting a broadly...