Australia RBA Cash Rate held at 3.60%

The RBA kept policy steady, reinforcing its patient stance as inflation trends lower but labour market conditions remain resilient. With unemployment stable and domestic demand moderating, the Board signalled it is comfortable staying restrictive for longer while assessing lagged policy impacts, keeping financial conditions tight as the outlook remains data-dependent.

United States JOLTS Job Openings beat at 7.67M

US job openings surprised to the upside, highlighting ongoing labour market tightness despite cooling activity elsewhere. The resilience in vacancies supports wage persistence risks and reinforces the Fed’s cautious approach to easing, suggesting labour rebalancing remains incomplete even as broader growth indicators soften.

China CPI rises to 0.7% vs 0.2% prior

Chinese inflation firmed meaningfully, easing immediate deflation concerns and suggesting policy stimulus is gaining traction. Improving price momentum may help stabilise corporate margins and household sentiment, supporting industrial demand and commodity imports as policymakers balance growth support with financial stability objectives.

United States Federal Funds Rate cut to 3.75% as expected

The Fed delivered a well-telegraphed rate cut, framing it as recalibration rather than the start of an aggressive easing cycle. Forward guidance emphasised optionality, with future moves contingent on inflation progress and labour cooling, reinforcing a gradualist outlook rather than a policy pivot.

Australian Unemployment Rate steady at 4.3%

Australian labour conditions remain stable, supporting household income resilience despite slowing growth. A steady unemployment rate reduces urgency for policy easing and aligns with the RBA’s wait-and-see approach, suggesting labour market softness is emerging only gradually as tighter financial conditions work through the economy.

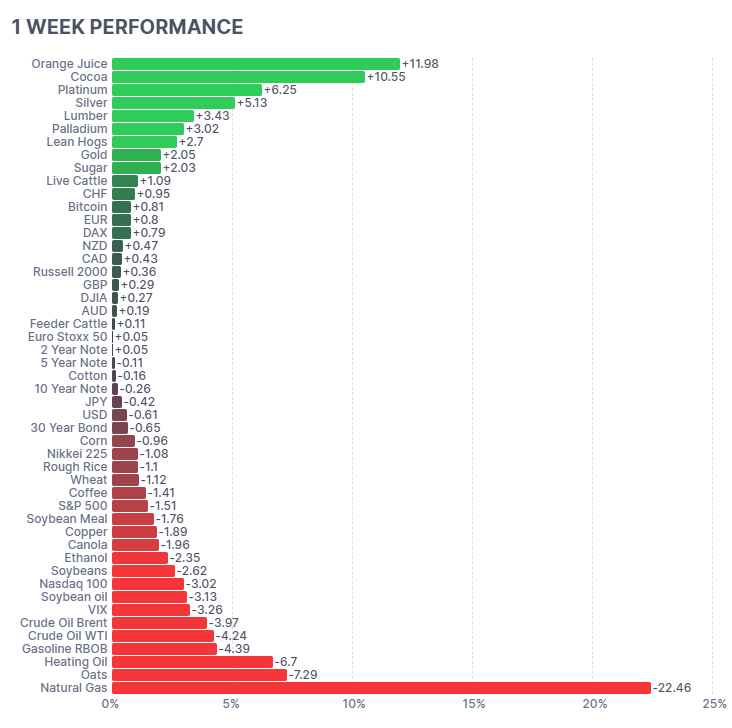

Below shows the monthly performance of a range of futures markets we track.

Commodity markets diverged sharply over the week, with softs and precious metals leading gains while energy and grains sold off. Orange Juice (+11.98%), Cocoa (+10.55%) and Platinum (+6.25%) surged on supply constraints and positioning dynamics, while Gold (+2.05%) remained supported by rate-cut confirmation. Energy markets were heavily pressured, with Natural Gas (-22.46%), Heating Oil (-6.70%) and WTI (-4.24%) sliding on oversupply and weaker demand expectations. Equity risk was mixed, with the S&P 500 (-1.51%) and Nasdaq 100 (-3.02%) under pressure as volatility rose (VIX +3.26%) amid sector rotation and rate repricing.

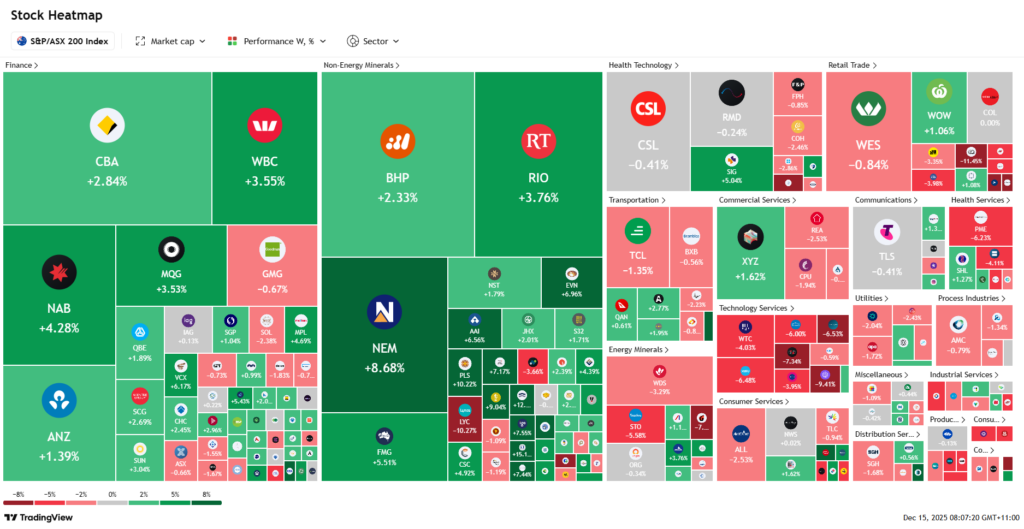

Here is the week’s heatmap for the largest companies in the ASX.

Australian equities were broadly constructive, driven by banks and large-cap resources. Financials outperformed, led by NAB (+4.28%), WBC (+3.55%) and CBA (+2.84%) as stable rates supported margins. Resource majors were firm, with BHP (+2.33%), RIO (+3.76%) and FMG (+5.51%) benefiting from improved China inflation data. Stock-specific strength was evident in NEM (+8.68%) and SIG (+5.04%), while technology and consumer names lagged, with WTC (-4.03%), XRO (-6.48%) and WES (-0.84%) reflecting earnings sensitivity and valuation pressure.

Related Insights

"US strikes on Iranian nuclear facilities drove oil prices sharply higher this week, while flat US c...

Iran's renewed blockade of the Strait of Hormuz reignited energy supply concerns this week, pushing...

US payrolls missed sharply at 57K this week, lifting rate cut expectations and supporting a broadly...